traveler1116

Introduction

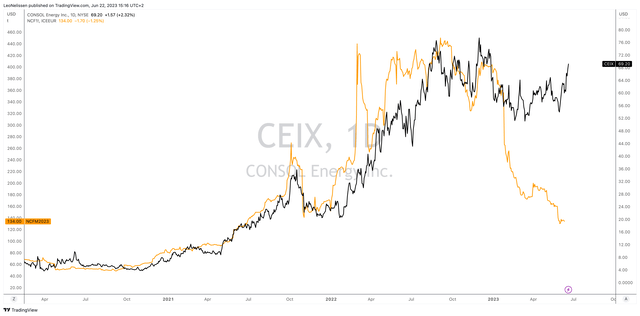

CONSOL Power (NYSE:CEIX) is defying gravity. Whereas the inventory hasn’t gone wherever for the reason that summer time of 2022, the coal miner is extraordinarily resilient, as its share worth is near its all-time excessive, regardless of large strain on coal costs.

The chart beneath exhibits the connection between CEIX and ICE Newcastle Coal futures, which I take advantage of as a benchmark for worldwide coal.

TradingView (CEIX, ICE Newcastle Coal)

On this article, we’ll dive into CEIX and the coal market to evaluate the danger/reward of present costs.

So, let’s get to it!

What Is CONSOL?

CONSOL Power has a $2.4 billion market cap, which makes it one of many largest North American coal producers. Headquartered in Canonsburg, Pennsylvania, CONSOL Power is a number one producer of high-quality bituminous coal. That is coal primarily used as thermal coal.

The corporate has a historical past that goes again to 1864 when it began as a coal producer within the Appalachian Basin. It turned an impartial, publicly-traded firm in 2017.

Now, the corporate’s core enterprise consists of three main pillars.

Pennsylvania Mining Complicated: The PAMC consists of the Bailey Mine, Enlow Fork Mine, Harvey Mine, and Central Preparation Plant. It has intensive reserves of high-quality coal and makes use of superior longwall mining techniques to attain excessive manufacturing volumes at low prices. CONSOL Marine Terminal: By way of its subsidiary, CONSOL Power gives coal export terminal providers on the Port of Baltimore. The terminal gives storage and loading amenities and advantages from being served by each Norfolk Southern (NSC) and CSX (CSX) railroads. Itmann Mining Complicated: The Itmann No. 5 Mine in West Virginia is designed to supply high-quality, low-volatile coking coal. The preparation plant has a rail loadout and the potential to course of extra tons from third-party sources, supporting the corporate’s development.

CEIX 2022 10-Ok

The newly constructed Itmann Preparation Plant started coal processing in late 2022 with the purpose of manufacturing high-quality, low-volatile coking coal. The advanced additionally features a rail loadout and has the potential to course of extra saleable tons from third-party sources, offering alternatives for development.

CEIX Is A Money Machine

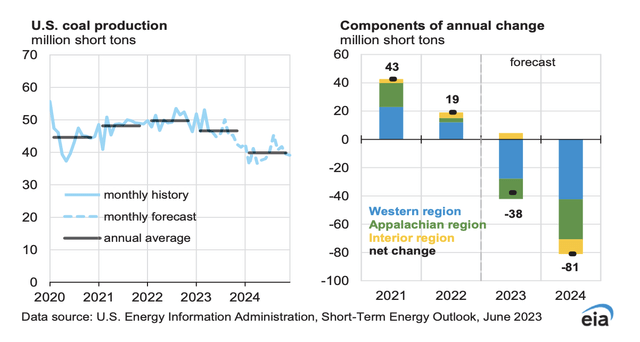

Because the chart within the introduction confirmed, coal is dealing with headwinds. The principle concern is slowing international financial development and the truth that the Northern Hemisphere had a really delicate winter, which brought about pure gasoline inventories to stay excessive. The dreaded winter after Russia shut down pure gasoline exports to Western Europe didn’t occur.

Power Data Administration

Based on the US Power Data Administration (“EIA”), the manufacturing of coal in america is predicted to fall by 6% in 2023, reaching roughly 560 million quick tons (“MMst”).

Moreover, the EIA predicts an additional decline of 14% in 2024, with coal manufacturing dropping to round 480 MMst.

This downward pattern is primarily brought on by a projected 19% discount in coal consumption by the electrical energy sector in 2023.

Nevertheless, the demand for coal from abroad markets is predicted to proceed offering help for US coal manufacturing via exports.

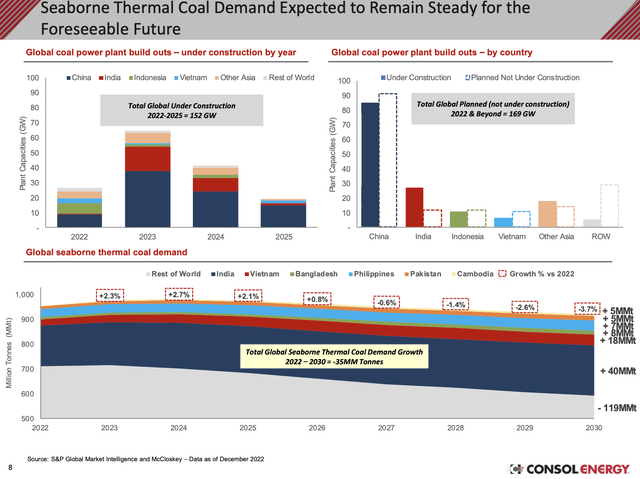

CEIX confirms this, because it highlights the large pipeline of recent coal merchandise in rising markets. I imagine that these developments may very well be additional fueled by a possible steep rise in pure gasoline and oil costs the second financial demand bottoms.

CONSOL Power

With that stated, regardless of international pricing and demand headwinds, CEIX is doing very nicely.

Within the first quarter of 2023, CEIX skilled a muted home coal burn as a result of aforementioned hotter winter and associated decline in pure gasoline costs.

Nevertheless, the corporate’s advertising group tailored and elevated its give attention to the export market, the place demand remained sturdy, notably within the industrial sector.

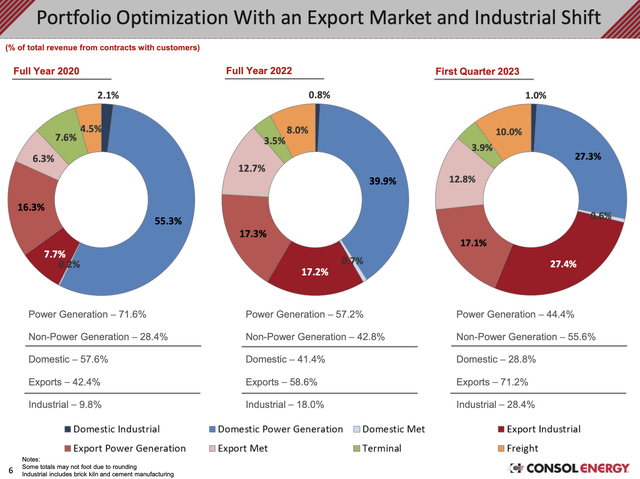

Therefore, CEIX achieved document gross sales of 6.7 million tons of PAMC coal, with a median realized coal income per ton offered of $84.32, in comparison with 6.5 million tons at $59.60 in the identical interval final 12 months.

Gross sales into the economic export market surpassed gross sales into the home energy era marketplace for the primary time within the firm’s historical past, which is a outstanding improvement.

Total, gross sales to the export market accounted for 66% of the full PAMC realized coal income, together with 33% from the economic export market and 13% from the export crossover metallurgical coal market.

These developments spotlight CEIX’s potential to leverage its export advertising and logistic benefits to offset weak spot within the home power markets.

The chart beneath exhibits that the corporate went from 42% export publicity in 2020 to 71% export publicity in 1Q23.

CONSOL Power

On condition that home demand is in a long-term secular downtrend, this potential is essential.

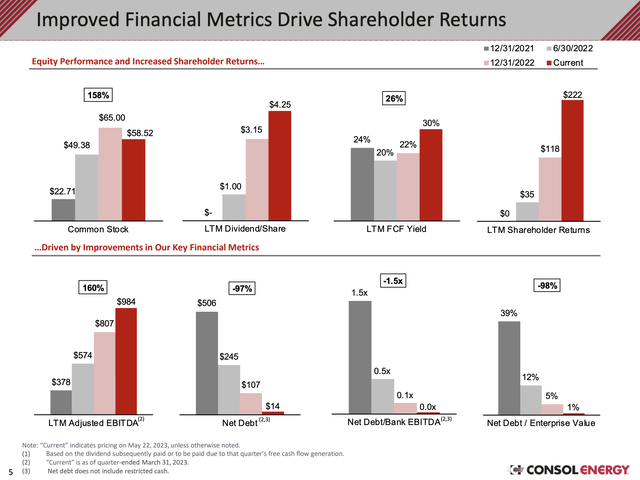

Consequently, CEIX reported a powerful monetary efficiency within the first quarter of 2023, with a web earnings of $230 million. This interprets to $6.55 per diluted share. It is also the corporate’s highest quarterly earnings per share degree for the second consecutive quarter.

Adjusted EBITDA got here in at $346 million, and free money stream reached $221 million.

What’s fascinating is not simply its stellar efficiency but in addition how the corporate is spending its free money. In spite of everything, like oil firms, most North American coal firms are actually in a lot better form and desirous to let shareholders profit.

Due to pricing and quantity tailwinds up to now few years, CEIX has made important progress in managing its stability sheet and capital allocation, which continued in the course of the first quarter of 2023.

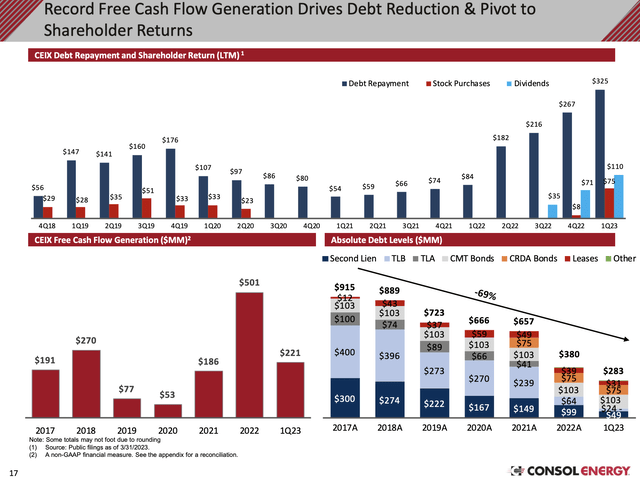

The corporate generated $221 million in free money stream, with roughly 45% of it used to additional scale back the gross debt degree. As of March 31, the full web debt stood at $14 million when factoring in unrestricted money and short-term investments. That is a 97% decline from 2021 ranges – as seen within the chart beneath.

CONSOL Power

CEIX additionally retired its Time period Mortgage B by making a $24 million discretionary cost and submitted a redemption discover for 25 million of its second lien notes, price a complete of $49 million.

These actions will carry the gross debt degree to round $240 million, and the corporate expects to completely retire the second lien notes quickly.

CONSOL Power

Moreover, CEIX maintained a powerful liquidity place of $384 million, regardless of a discount within the revolving credit score facility borrowing restrict.

Moreover, the corporate repurchased 1.2 million shares of its excellent widespread inventory for $67 million and introduced a dividend of $1.10 per share (6.7% yield).

CONSOL Power

The overview above completely exhibits the corporate’s accelerating pattern in debt repayments and share repurchases.

Share repurchases are actually anticipated to speed up.

Due to the close to completion of its debt discount targets, CONSOL Power is now dedicated to returning a good portion of its quarterly free money stream to shareholders.

The corporate introduced a rise to its enhanced shareholder return program, efficient in 2Q23.

Primarily, CONSOL Power plans to return 75% of quarterly free money flows to shareholders. The main focus of its return program will shift primarily to share buybacks as a substitute of dividends. This resolution relies on the enticing free money stream yields at which the corporate’s inventory is buying and selling, the tax effectivity of buybacks, and suggestions from its shareholder base.

In different phrases, CEIX believes that its inventory is severely undervalued, which makes buybacks far more enticing than dividends.

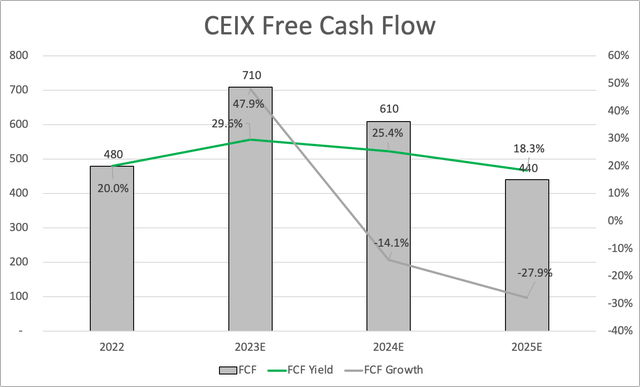

Taking a look at free money stream yield estimates, we see that even when free money stream falls to $440 million in 2025 (analysts are pricing in coal worth normalization and decrease home demand), the corporate would nonetheless have an 18% FCF yield.

Leo Nelissen

In different phrases, if the market cap have been to stay unchanged, the corporate may purchase again 18% of its shares while not having debt or neglecting its operations. This quantity excludes the dividend. If the dividend have been 8%, buybacks may nonetheless be 10%.

That is a surprising quantity.

It additionally explains why CEIX has performed relatively nicely, regardless of the implosion in worldwide coal futures like ICE Newcastle.

It additionally helps the valuation. The inventory is buying and selling at lower than 4x 2023/2024 anticipated free money stream.

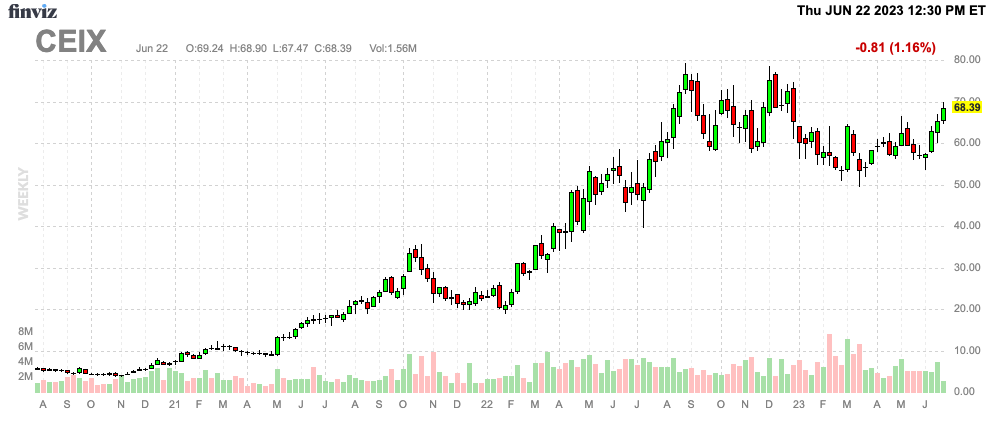

FINVIZ

The present consensus worth goal is $80, which suggests an 18% upside. I agree with that.

Nevertheless, I don’t urge buyers to purchase at these costs. Given the volatility and financial dangers, I’d solely purchase CEIX on a steep sell-off.

Moreover, I’ve a correlated play, as I not too long ago entered into a big pure gasoline commerce. If my pure gasoline thesis is appropriate, CEIX will profit as nicely.

With that stated, whereas I’ll give CEIX a bullish ranking due to my perception that coal demand and costs can be increased for longer, I’m not encouraging folks to purchase cyclical coal publicity. Solely take into account shopping for it in case you’re acquainted with unstable belongings and conscious of the drivers behind coal costs.

Additionally, be sure to attend for a correction. I would not purchase after the current rally.

Takeaway

Regardless of the difficult surroundings for coal, CONSOL Power has proven outstanding resilience and powerful monetary efficiency. With a give attention to the export market and leveraging its advertising and logistic benefits, CEIX has managed to offset weak spot within the home power markets.

Moreover, the corporate’s potential to generate free money stream and successfully handle its stability sheet is spectacular, leading to important debt discount and shareholder worth creation.

Therefore, CEIX plans to speed up share buybacks, contemplating its inventory to be undervalued.

Whereas the inventory at the moment trades at a lovely valuation, warning is suggested attributable to volatility and financial dangers.

Traders ought to take into account shopping for on a steep sell-off and pay attention to the elements influencing coal costs.

Total, CEIX’s efficiency and potential warrant consideration, however prudent timing and understanding of the market are important.

{kind=link}