MadamLead

Duff & Phelps is a well-liked fund supervisor in utility and infrastructure fairness CEFs although it shocked everybody final week when the Duff & Phelps Utility & Infrastructure Fund (NYSE:DPG), $9.50 actual time market value, -1.7%, minimize its distribution by -40% final Thursday when the fund reached a comparatively excessive 12.5% NAV yield as a result of a tough atmosphere for utility shares.

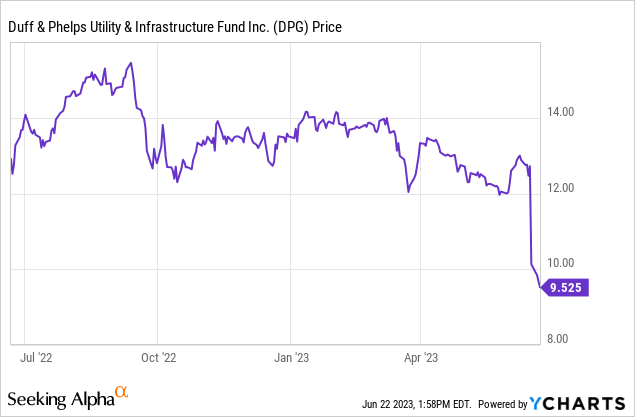

Consequently, DPG dropped -20.4% final Friday and remains to be in free fall as shareholders have misplaced confidence and have deserted the fund. As of two EST PM in the present day, DPG has dropped to as little as $9.42 and can most likely be round a -15% low cost after in the present day.

This is a 1-year MKT value of DPG:

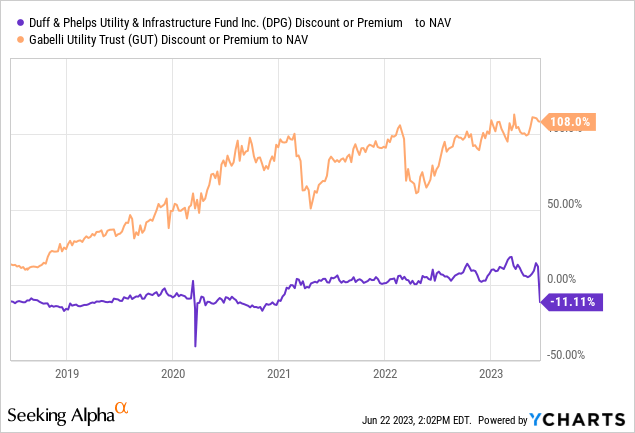

However, one other utility targeted CEF, the Gabelli Utility Belief (GUT), $6.87 present market value, can in some way keep a +110% market value premium, with an 18.4% NAV yield.

Does this make any sense in anyway? Each funds focus in the identical utility sectors and shares and what they do not overlap in tends to be a few of their smaller sector weightings.

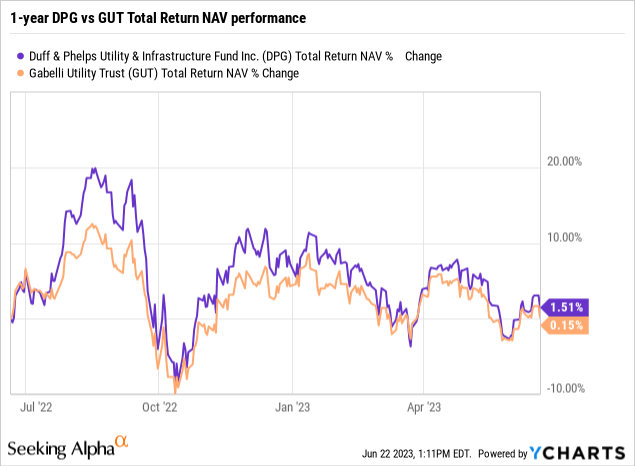

Consequently, each DPG and GUT have had very comparable NAV whole return performances over the previous yr.

So how is it that DPG, with a excessive 12.5% NAV yield as of final week, felt the necessity to have to chop its distribution and is now at a way more cheap and achievable 7.5% NAV yield, however but GAMCO does not minimize GUT’s distribution even at an astronomically greater 18.4% NAV yield?

This is a three-year Premium/Low cost chart of DPG and GUT:

It is one of the vital inexplicable valuation variations I’ve ever seen amongst CEFs that focus in comparable sectors, made much more ridiculous by the truth that each funds have a variety of overlap of their portfolios, particularly in utility shares which make up their highest sector publicity in every fund.

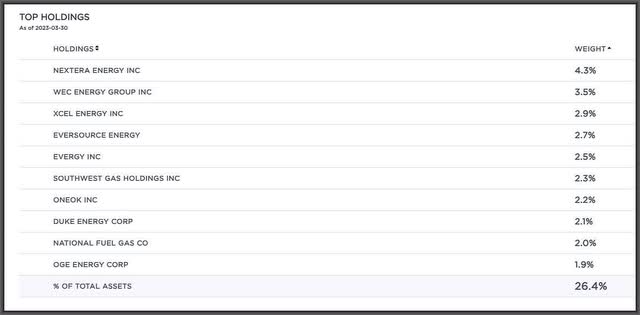

Listed below are GUT’s high 10 holdings as of three/30/23:

Gabelli

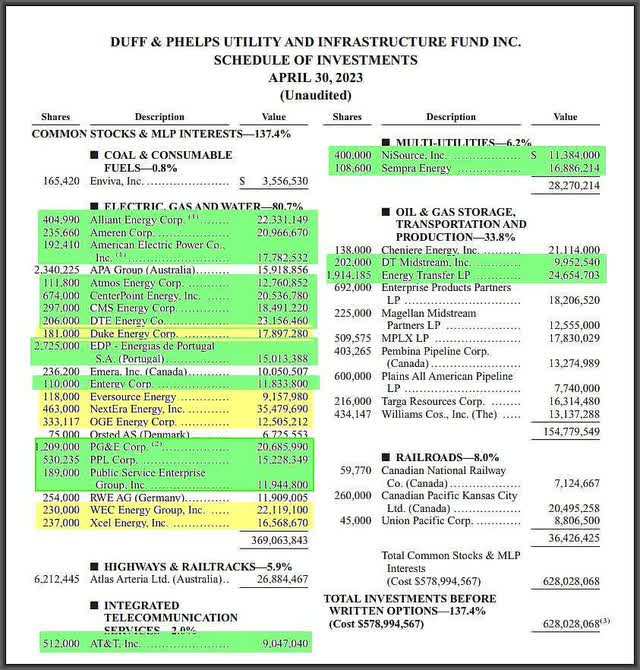

And listed here are all of DPG’s holdings as of 4/30/23:

Duff & Phelps

Yellow represents high 10 holdings of GUT which can be additionally owned by DPG and there are a complete of six, together with NextEra Power (NEE), which is the highest holding in each funds and WEC Power (WEC), which is in each fund’s high 10 holdings.

Then inexperienced represents firms which can be owned in each funds, lots of that are massive positions as properly. I did not calculate the whole proportion overlap, however it’s undoubtedly a big proportion.

Word: I am not exhibiting all of GUT’s positions because it covers a number of pages however if you’re fascinated by seeing all of GUT’s holdings as of first quarter 2023, click on right here

So the query is, why does DPG minimize when GUT, which is clearly overpaying its distribution by a a lot greater margin, does not? I am unable to say what motivates GAMCO for not chopping GUT’s distribution by now, however clearly, DPG’s valuation is dramatically extra engaging than GUT’s at this level.

I didn’t personal DPG earlier than final Thursday’s distribution minimize declaration, and I waited to provoke a place till Tuesday of this week at $9.77.

That mentioned, shareholders proceed to rid themselves of shares. However I imagine that is WAY overdone at this level, particularly when GUT is now the fund that basically needs to be within the crosshairs of shareholders.

I’ve added to my place in DPG as little as $9.41 in the present day.

{kind=link}