J. Michael Jones

Synovus Monetary Corp. (NYSE:SNV) operates as a financial institution holding firm for Synovus Financial institution; it was based again in 1888 and is headquartered in Columbus, Georgia.

TradingView

Regardless of a slight restoration in current weeks, the results of the banking crises triggered by SVB’s chapter are nonetheless being mirrored within the value of Synovus Monetary, which is certainly removed from its all-time excessive. Nonetheless, such a decline has revealed alternatives that weren’t there earlier than, together with a dividend yield of 4.80%.

As I’ll present you all through this text, at this value Synovus Monetary could also be choice, particularly for these searching for excessive and sustainable dividends. However it’s most likely not for me.

Deposits High quality

For my part, deposits high quality is the primary side to contemplate when analyzing a financial institution, as it’s the uncooked materials on which all the monetary construction relies. I’ll now present you ways Synovus Monetary is positioned on this respect.

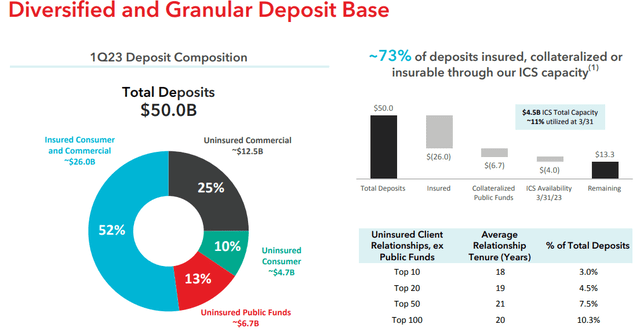

Synovus Monetary Corp Q1 2023

Initially, about 73 p.c of deposits are insured, collateralized or insurable. The deposit base is each diversified and never very concentrated, which is optimistic. In reality, the highest 100 uninsured prospects account for simply over 10 p.c of complete deposits.

Synovus Monetary Corp Q1 2023

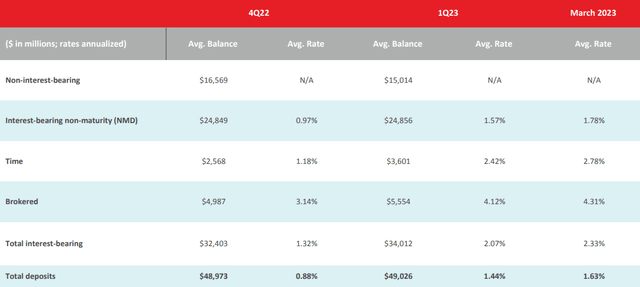

In all probability the least optimistic side issues the price of deposits, in reality in March 2023 the typical curiosity paid was 1.63% when only some months earlier it was 0.88%. As well as, additionally it is vital to say that non-interest-bearing deposits have decreased by $1.55 billion in comparison with This autumn 2022, which is certainly an element to contemplate. Synovus Monetary has needed to discover different methods to interchange these free funds, together with time deposits and brokered CDs, each of that are considerably costlier. Combining each deposits and loans, the general common value amounted to 2.33 p.c in March, 101 foundation factors greater than in This autumn 2022.

Synovus Monetary Corp Q1 2023

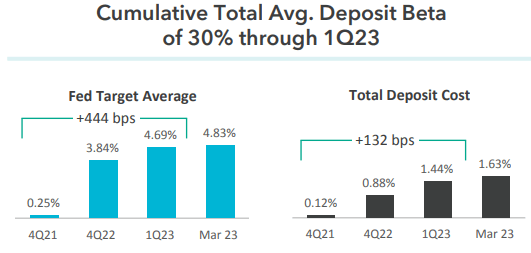

Evaluating the rise within the Fed Funds Price and the price of deposits, Synovus Monetary was in a position to obtain a deposit beta of 30 p.c, which is an honest outcome however definitely not optimum. In keeping with the most recent Fed estimates, we are able to anticipate not less than two extra 25 foundation level hikes by the top of the yr, which might imply that the deposit beta might proceed to rise.

Over the previous month I’ve been analyzing many regional banks, and Synovus Monetary reveals common outcomes when it comes to deposit prices; nothing worrisome however nothing thrilling both. For instance, there are banks like Banner that haven’t been affected as a lot by the rate of interest improve; in reality, it nonetheless displays a deposit value of lower than 0.30 p.c.

Incomes Asset Composition and Internet Curiosity Margin

The deposits value shouldn’t be the one issue that adjusts for rates of interest; there may be additionally the yield on property.

Synovus Monetary Corp Q1 2023

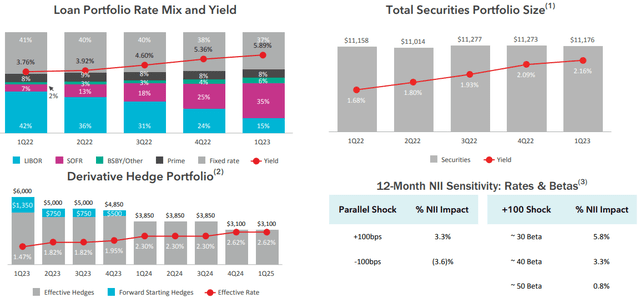

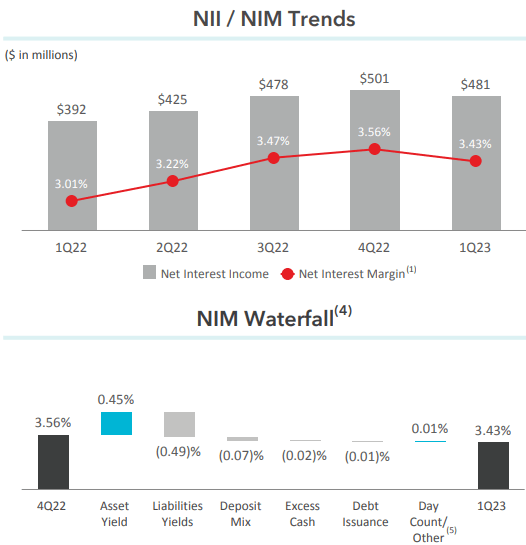

The mortgage portfolio fee steadily elevated every quarter and reached 5.89 p.c, which makes the rise in the price of liabilities much less bitter. On the identical time, the securities portfolio additionally introduced a progress in yield, though its measurement remained virtually unchanged from Q1 2022.

Though not featured on this slide, with regard to the securities portfolio it ought to be identified that, as of Q1 2023, it’s registering an unrealized lack of as a lot as $1.28 billion, a considerably giant determine. In reality, it represents about 27 p.c of fairness. Synovus Monetary, in addition to many different banks, made main purchases of fixed-rate securities earlier than the Fed aggressively raised rates of interest, and this led to a big unrealized loss, particularly for prime period securities. If the Fed had been to chop rates of interest lots, the issue would recede: the purpose is that earlier than 2024 it’s unlikely to occur. So, so long as the macroeconomic situation stays the identical, we’ve to contemplate this huge unrealized loss in Synovus Monetary’s steadiness sheet. The latter, after all additionally weighs on the E book Worth per share, a key metric to which every financial institution’s value per share follows.

Staying with rate of interest danger, within the final slide we are able to see the anticipated change in internet curiosity revenue (NII) as rates of interest change. A 100-basis level improve would have a +3.30 p.c impression on NII; a 100-basis level lower would have a – 3.60 p.c impression. Briefly, the financial institution is positioned towards an extra improve in rates of interest. Thus, ought to the Fed cut back them, on the one hand the unrealized lack of the securities portfolio could be lowered, however alternatively the NII would endure.

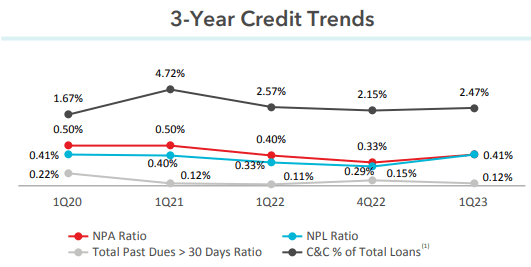

Synovus Monetary Corp Q1 2023

Returning briefly to the mortgage portfolio, we are able to see that in the meanwhile the principle indices used for credit score danger are all in good standing. So, regardless of Synovus Monetary’s vital publicity to the CRE section, in the meanwhile, there isn’t any motive to doubt the creditworthiness of its debtors.

In any case, though the yield on property has improved, it has not been in a position to absolutely cowl the rise in the price of liabilities. In reality, the online curiosity margin decreased by 13 foundation factors in comparison with This autumn 2022.

Synovus Monetary Corp Q1 2023

Asset yield affected +0.45%, but it surely was not sufficient towards – 0.49%. As well as, extra money and deposit combine additionally didn’t assist Synovus Monetary; – 0.02% and – 0.07% respectively.

Dividend Evaluation

As anticipated originally of the article, the dividend yield of Synovus Monetary appears engaging for individuals who want to spend money on corporations with a excessive dividend yield; on this case, we’re speaking about 4.80%. However is it sustainable?

Searching for Alpha

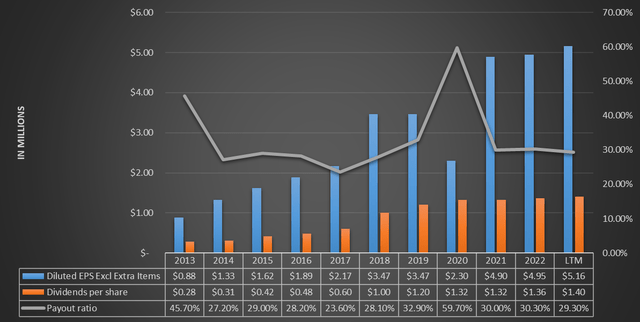

Evaluating diluted EPS with dividend per share, it’s evident that the previous are considerably larger than the latter. In reality, the payout ratio is sort of low, solely 29.30 p.c. So even when EPS slows down within the coming years as a result of long-awaited recession, in my view, administration will proceed to difficulty dividend anyway. In spite of everything, Synovus Monetary has a dividend yield of 4.80 p.c with a payout ratio of 29.30 p.c; if EPS dropped even 20-30 p.c, the payout ratio would nonetheless be lower than 50 p.c.

Briefly, barring any sensational unexpected occasions, I take into account the dividend to be sustainable within the coming years.

Searching for Alpha

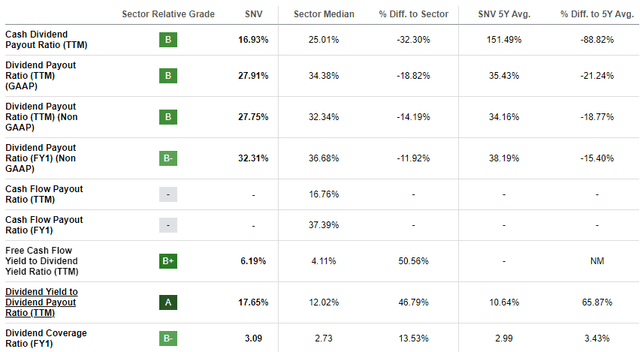

Lastly, in response to Searching for Alpha’s information on the dividend security, Synovus Monetary’s ratios are sometimes higher than its friends. Briefly, not less than for the second the state of affairs is steady.

Valuation

To evaluate the truthful worth of Synovus Monetary, I’ll use a weighted common amongst three valuation strategies; the primary may have a weight of 40% and can be primarily based on e-book worth, the second may have the identical weight however can be primarily based on EPS, and the third can be a dividend low cost mannequin with a weight of 20%. All information can be obtained from Searching for Alpha.

The typical value/e-book worth during the last 5 years is 1.31x; multiplying this determine by the present e-book worth per share of $28.98 leads to a good worth of $37.96 per share. The typical P/E for the previous 5 years has been 10.82x; multiplying this determine by the anticipated EPS for 2023 of $4.73 (Avenue estimates), the truthful worth quantities to $51.17 per share. As for the dividend low cost mannequin, the inputs can be as follows: Annual Payout (FWD) of $1.52 per share. Annual return required from the funding 15%. We’re speaking a few small regional financial institution, and being a really dangerous funding, in my view a excessive return is required to take this danger. Dividend progress of 8% per yr. Over the previous 10 years the CAGR has been 17.79%, nevertheless I needed to incorporate a extra conservative worth. In spite of everything, the macroeconomic atmosphere has positively modified from 10 years in the past.

The ensuing truthful worth following these assumptions is $23.45 per share.

Summing it up, the primary two strategies present that Synovus Monetary is undervalued, particularly the one with earnings, whereas for the dividend low cost mannequin this financial institution is overvalued. Within the final technique, the required return positively affected lots, however I feel it’s unavoidable given the riskiness of the funding.

By making the weighted common of the three fashions in response to the instructions I discussed earlier, the truthful worth of Synovus Monetary is $40.34 per share, so the inventory is undervalued.

Last Ideas

Total, Synovus Monetary is a financial institution that has suffered from the rising value of deposits and this has affected the online curiosity margin. Unrealized losses are one other difficulty to observe, however I stay optimistic as a result of when the Fed reduces rates of interest this loss will disappear. In the meanwhile, the market is discounting these points within the value of Synovus Monetary, which is why it seems slightly at a reduction. So, the inventory is undervalued, the dividend is excessive, however why do not I spend money on it?

The reason being that like Synovus Monetary, many different regional banks are in the same state of affairs, which leads me to keep away from investing in them. Quite than make investments individually in all these banks with comparable traits and issues, I want to purchase an ETF. If I’ve to spend money on a single financial institution, I would like it to have peculiarities which can be out of the unusual. On this regard, I recommend you learn my article on Banner Company, a semi-unknown financial institution that I imagine might mirror the latter description.

{kind=link}