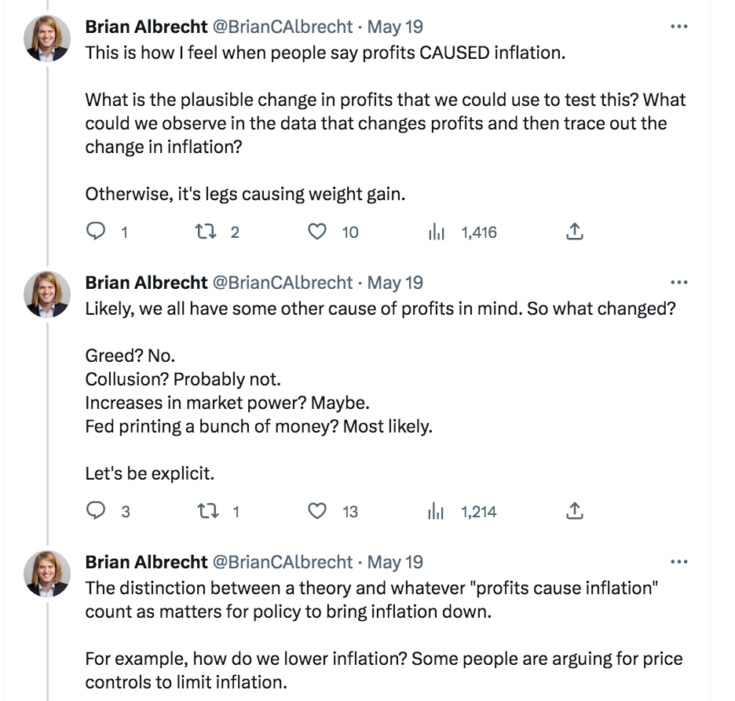

Brian Albrecht has a intelligent sequence of tweets evaluating inflation and weight acquire:

After a sarcastic remark about reducing off legs to drop a few pounds, Albrecht then attracts some coverage implications:

I’d prefer to take this analogy a bit additional. I can think about a number of instances the place it would make sense to attribute weight acquire to a selected a part of the physique. Suppose all the weight acquire occurred within the decrease torso, as a consequence of a cancerous tumor. In that case, a health care provider would possibly suggest that the affected person not attempt to drop a few pounds in different components of the physique to offset the acquire within the decrease torso. In that case, it would make sense to talk of a tumor as inflicting weight acquire.

Usually, nonetheless, weight acquire is brought on by consuming an excessive amount of meals (mixed with not sufficient train.)

Most critical bouts of inflation are brought on by extreme mixture demand—excessively speedy progress in nominal GDP. That is equal to extreme consumption of meals. In some instances, nonetheless, temporary durations of inflation can happen as a consequence of issues in a selected space of the economic system, with none improve in NGDP. An oil shock would possibly elevate costs and decrease output by an equal quantity. More and more monopolistic firms would possibly scale back output to drive up costs. More and more highly effective labor unions would possibly scale back the entire workforce to drive up wages.

In that case, a “financial physician” would possibly recommend not offsetting value will increase in a single sector with deflation in one other. As an alternative, it is perhaps higher to permit a short lived rise in inflation, so long as NGDP progress stays on monitor. This might be like permitting some weight acquire from a tumor.

In fact that doesn’t imply {that a} tumor just isn’t an issue, quite that weight-reduction plan just isn’t the optimum resolution to most cancers. As an alternative, you would possibly strive radiation or chemotherapy. Equally, my declare just isn’t that provide shocks usually are not an issue; quite the declare is that the ensuing rise within the CPI is in some sense optimum, given the existence of the availability downside. Chances are you’ll want to use different coverage instruments to spice up mixture provide.

I see numerous confusion when individuals converse of inflation being brought on by “provide bottlenecks”, or “greed”, or “rising wages”, or “price range deficits”, or “forex depreciation”. What are the related coverage counterfactuals? What do you imply by “trigger”? Simply because costs rise earlier than wages doesn’t suggest that costs trigger wages.

That is from a latest paper by Norbert Michel and Jai Kedia:

Past these easy comparisons of percentages, extra subtle analysis suggests that there’s little purpose to anticipate financial coverage to have a lot of an impact on costs within the providers business. As a Cato research utilizing a VAR method finds, Fed coverage has hardly mattered in explaining inflation (providers or in any other case). Determine 1 beneath reproduces the breakdown of inflation into its demand, provide, and financial coverage elements from 1960 onwards. Because the graph exhibits, provide components dominate – they account for over 80% of the variation in service‐sector inflation, each within the brief‐time period and lengthy‐time period. Within the close to time period, financial coverage explains lower than 2% of inflation. In the long run, the results improve however by no means account for greater than 5% of service‐sector inflation.

VAR research aren’t going to inform you something about inflation causation, no less than in any commonsense which means of the time period “trigger”.

In my opinion, nearly all the inflation since 1960 has been as a consequence of financial coverage. If actual GDP grows at 3% since 1960, and nominal GDP grows at 7%, then you definitely’ll have a 4% common inflation fee. Financial coverage drives NGDP progress, and therefore explains the surplus of NGDP over RGDP progress. With much less expansionary financial coverage we’d have had much less inflation (each complete and providers.) Moreover, financial coverage just isn’t another concept to “demand”, it’s what determines demand. When you’ve remoted the availability and demand “elements”, there’s nothing left.

Brian Albrecht is strictly proper when he means that in economics it’s most helpful to consider causation when it comes to coverage counterfactuals:

I don’t wish to get into semantic disputes, however a concept of inflation needs to be *causal*. A causes inflation typically. B brought on inflation right here. On the coronary heart of causation is the counterfactual. If X had been totally different, then Y would have been totally different.

It’s theoretically potential that our latest inflation was brought on by one thing aside from financial coverage, reminiscent of elevated greed, or more and more highly effective labor unions. But it surely simply so occurs that the latest overshoot of NGDP progress is sort of much like the latest overshoot of inflation. That signifies that on this case the trigger is just “overeating”, no want to go looking out mysterious “tumors” within the physique.

My daughter lately despatched me a San Francisco Fed paper by Adam Hale Shapiro trying on the impact of wage inflation on total inflation. The summary suggests little impression:

Labor-cost progress has no significant impact on items or housing providers inflation. General, labor-cost progress is answerable for solely about 0.1 proportion level of latest core PCE inflation.

The opening paragraph quotes Jay Powell:

In a November 2022 speech, Federal Reserve Chair Jerome Powell talked about that it’s useful to elucidate elevated inflation ranges by inspecting three underlying classes: items, housing providers, and nonhousing providers. He paid explicit consideration to the final class, stating that it “could also be a very powerful class for understanding the long run evolution of core inflation. As a result of wages make up the biggest price in delivering these providers, the labor market holds the important thing to understanding inflation on this class” (Powell 2022).

And Shapiro concludes as follows:

As an example, latest proof exhibits that wage progress tends to comply with inflation, in addition to expectations of future inflation (Glick, Leduc, and Pepper 2022). General, the outcomes spotlight that latest labor-cost progress is more likely to be a poor gauge of dangers to the inflation outlook.

I think that some readers would possibly conclude that Shapiro is contradicting Powell. However I don’t see it that method—I believe they’re each appropriate. Wages usually are not inflicting inflation. Wages don’t predict adjustments within the path of core inflation. However there’s a sense that wages are the essence of the present inflation downside (as Powell is implicitly suggesting.)

Right here’s how I take a look at inflation. An optimum financial coverage (say 3.5% NGDP progress) would result in regular nominal wage progress at about 3%/12 months. Due to productiveness progress of roughly 1%, that can ship 2% inflation, on common. Precise inflation will fluctuate as a consequence of provide shocks. However any durations of above 2% inflation shall be “transitory”, so long as financial coverage retains nominal wages rising at 3%. And never simply transitory; the surplus inflation may even be applicable—that’s, higher than the choice of forcing down some costs to offset spikes in different costs.

The truth that nominal wage progress has risen to roughly 5% is a sign that financial coverage has been too expansionary. The ensuing inflation just isn’t transitory, and received’t go away by itself. It should take a financial coverage that’s tight sufficient to no less than considerably depress the labor market. (Hopefully not excessive sufficient to trigger a big recession.) We have to get wage progress down to three%.

When financial coverage is simply too expansionary, the results present up first in versatile costs and nominal GDP. Nominal wages reply with a lag. Thus in any statistical take a look at it received’t seem like wages are inflicting inflation. However as a result of secure wage progress is a roughly optimum financial coverage, wages are in a way the essence of the inflation downside, with out being the trigger.

I’m struggling to consider an analogy with weight acquire, however let’s suppose that when consuming an excessive amount of the burden first went to your abdomen, after which later to your thighs. Additionally suppose that it’s simpler to get the burden again down when it’s nonetheless in your abdomen, however tougher as soon as it provides to your thighs. Extreme wage progress is kind of just like the fats thighs; as soon as wages start rising too quick it’s tougher to scale back inflation with out a recession.

The query of causation in macroeconomics is trickier than many individuals suspect. Economists that I respect will say, “It’s foolish to say inflation is brought on by hovering oil costs, as rising costs are the definition of inflation. That’s like saying inflation is brought on by inflation.” Sure, but it surely’s additionally true that beneath sure applicable financial coverage regimes, sure varieties of provide shocks can create short-term inflation. All these latest theories of bottlenecks, greed, and wages inflicting inflation aren’t incorrect as a result of they will’t be proper, they’re incorrect as a result of they don’t occur to be proper on this case—it’s nearly all extra NGDP progress (since 2019).

As a rustic we ate an excessive amount of, gorging on financial stimulus. And now we have to sacrifice with an disagreeable interval of weight-reduction plan.

.jpeg?itok=EJhTOXAj'%20%20%20og_image:%20'https://cdn.mises.org/styles/social_media/s3/images/2025-03/AdobeStock_Supreme%20Court%20(2).jpeg?itok=EJhTOXAj)

{kind=link}