Scott Olson/Getty Photographs Information

Background

Warren Buffett constructed his chops by following the investing tenets of his mentor, Benjamin Graham. Early on, his philosophy was simple–find firms which might be very cheaply priced relative to their belongings, purchase them, and maintain till the market realized their intrinsic worth in a technique or one other and the value went up. This was the so-called ‘cigar butt’ type of investing. It wasn’t till Buffett met his long-time companion Charlie Munger that the method to investing modified. Somewhat than discovering firms that had been buying and selling extraordinarily cheaply, Munger insisted that they deal with high-quality firms with a large aggressive moat that could possibly be sustained over lengthy intervals of time.

With Johnson & Johnson’s (JNJ) current spinoff of Kenvue (NYSE:KVUE), we imagine traders of a sure sort have been introduced simply this type of latter, Munger-and-Buffett-esque alternative.

Let’s dive in.

Every thing You Want, Nothing You Do not

First, some fundamentals. Debuting in its IPO on Might 4th, 2023, Kenvue is a derivative of Johnson & Johnson and accommodates the guardian firm’s client well being merchandise. The merchandise in its portfolio are family names: Tylenol, Band-Assist, Sudafed, Motrin, and Neutrogena to call just a few. The brand new firm operates in three segments, Self Care, Pores and skin Well being and Magnificence, and Important Well being. The guardian firm at the moment retains nearly 90% of Kenvue, though Johnson & Johnson has acknowledged that its intent is the distribute this fairness to its shareholders (the time-frame for this distribution is unclear, nevertheless, and the primary Kenvue 10Q factors out that Johnson & Johnson is beneath no obligation to really distribute the shares if it so chooses). Kenvue additionally plans to pay out an annualized dividend of roughly 3.7% to shareholders.

Earlier than the spinoff, one of many major–and most worrying–questions that traders had involved Johnson & Johnson’s ongoing authorized troubles relating to its talc product (the corporate’s child powder merchandise now belong to Kenvue). This concern, nevertheless, will be kind of put to relaxation. Johnson & Johnson CFO Joe Wolk acknowledged definitively within the newest convention name that because it considerations ongoing litigation relating to talc, “the talc liabilities in america and Canada will stay with Johnson & Johnson.” Kenvue will, as Wolk’s assertion implies, retain legal responsibility for any arising lawsuits exterior the U.S. or Canada.

Whereas it could possibly be argued that Johnson & Johnson did not have a lot of a selection about retaining the North American legal responsibility (in any case, 3M (MMM) tried to, and was blocked from, shifting legal responsibility for its notorious earplug lawsuits to a derivative entity), we expect that the shortage of an try and shift legal responsibility remains to be vital, since it’s not all the time the coverage of the guardian firm to arrange the corporate to be spun off for achievement.

Following this theme of company accountability, Kenvue is well-capitalized and didn’t bear an extreme burdening of debt that’s so typically a function of spinoffs.

Firm Filings

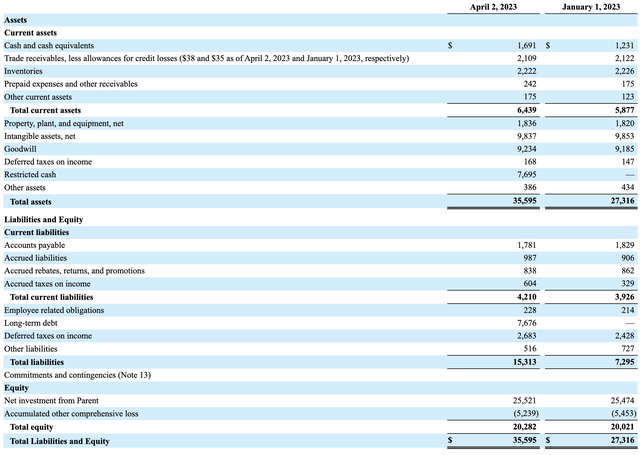

Kenvue at the moment boasts a wholesome $20 billion in fairness, with $35 billion in belongings in opposition to $15 billion in debt. Annualized run fee income primarily based on the primary quarter stands at $15.2 billion, and the annualized run fee working money move is a formidable $3.2 billion.

Buffett Model

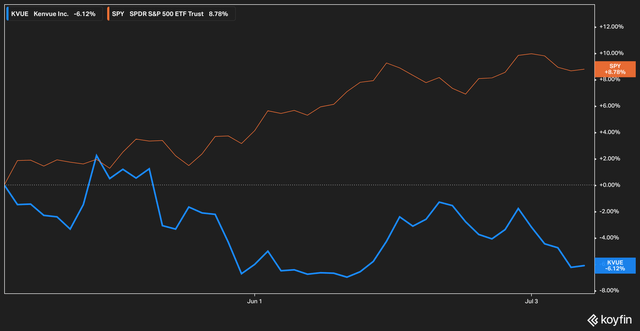

Kenvue has underperformed the market in its first few months as a public firm. This isn’t trigger for alarm–large company spinoffs can endure occasions of underperformance following separation from the guardian firm as shareholders who’ve simply obtained fractional shares of the brand new firm are inclined to shed them from their portfolio. Whereas Johnson & Johnson nonetheless retains a big majority of shares, distributions are seemingly in our opinion to place some downward stress on the inventory within the close to time period.

Koyfin

For extra context on how the difficulty could carry out in the course of the first yr of its public life, we flip to competitor Haleon (HLN), which was the patron well being unit of GSK plc (GSK) and was spun out of the guardian firm in mid-2022. Within the first six months of its public itemizing, Haleon dipped by as a lot as 25% earlier than recovering and climbing above its IPO worth.

Given the character of the merchandise it sells, nevertheless, we view dips in Kenvue’s share worth as compelling alternatives to purchase. With a steady of family identify merchandise, the necessity for continuous repeat purchases by customers, and regular, rising demand (extra on that later), we expect that Kenvue gives a compelling, Warren Buffett type enterprise that may be purchased a comparatively low valuation in the present day.

Contemplate Buffett’s funding rationale for his long-term possession of Coca-Cola (KO). The corporate sells a big selection of drinks with a excessive diploma of brand name loyalty and a number of repeat purchases. Whereas our thesis mirrors this method, we additionally take note of that the merchandise bought by Kenvue are true client wants versus discretionary. For us, this provides an extra layer of attractiveness.

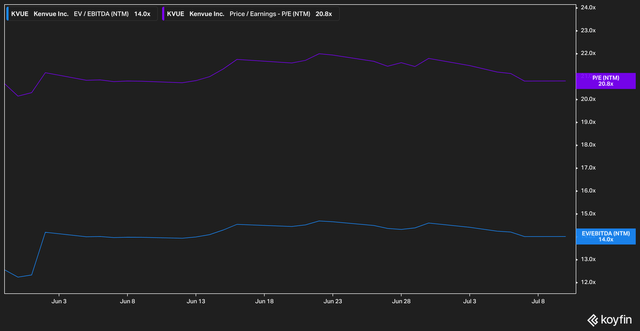

The present valuation of Kenvue additionally appears eminently affordable.

Koyfin

On a ahead foundation, the inventory at the moment trades fingers at 20x earnings and 14x EV/EBITDA. Whereas these multiples are barely increased than competitor Haleon’s, we level out that the stability sheet at Kenvue is superior, and that Kenvue has a extra compelling plan to return money to shareholders (Kenvue’s deliberate dividend yield is, once more, 3.7% whereas of this writing Haleon’s dividend yields 0.71%).

Buyers may be involved about stagnant growth–after all, there are solely so many Band-Aids and Tylenol a family should purchase, and solely so many households to buy stated objects. On this entrance, nevertheless, there may be motive to imagine that those that assume progress might be stagnant are incorrect. The healthcare agency IQVIA (IQV) revealed a report outlining the case that the over-the-counter drug market is forecast to develop by 6.1% by means of 2025, markedly higher than the three% world GDP forecast for 2024 revealed by the Worldwide Financial Fund.

The Backside Line

With family identify merchandise which might be extremely regarded by customers, a robust stability sheet, and wholesome forecasted progress in its addressable market, we imagine that Kenvue presents a compelling alternative for traders. Dangers to our thesis embody a doable recession which may affect even brand-loyal customers to modify to generic merchandise and execution threat from administration in implementing progress plans. We predict that these dangers, nevertheless, don’t outweigh the potential advantages of our thesis.

{kind=link}