Richard Drury

Enterprise Merchandise Companions (NYSE:EPD) simply proved as soon as once more why it is a midstream favourite among the many investing group. EPD has reached an vital milestone, as this 12 months marks the twenty fifth consecutive 12 months of annual distribution progress. EPD elevated the Distribution in Q1 of 2023 by 3.16%, going from $0.475 to $0.49, and simply offered unit holders with a further 2% distribution enhance in Q3. EPD shall be rising the upcoming distribution from $0.49 to $0.50 per unit, taking the annual distribution to $2. Based mostly on the brand new payout, EPD is now yielding 7.56%, and continues to be a champion of distributions for its traders. Investing in power is not thrilling to many traders, however midstream operators are identified for producing giant quantities of earnings. Whereas EPD would not generate the biggest yield of its friends, in my view, its distribution is of the best high quality as they by no means appear to disappoint with a steady circulate of will increase. When you’re in search of earnings, EPD is a high contender because it’s knocking on the door of changing into a Dividend Aristocrat.

Looking for Alpha

EPD has been a champion of earnings for greater than twenty years and the distributions simply get greater

Over the previous twenty years, we’ve got been by way of a monetary disaster, a mortgage disaster, recessions, an oil worth implosion, wars, and a pandemic. Regardless of uncontrollable components which have financial implications, EPD has by no means missed a quarterly distribution cost and has by no means lower or lowered the distribution. There are numerous corporations with excessive yields, and whereas I’m a unitholder of Power Switch (ET) and a shareholder of Kinder Morgan (KMI), they have been pressured to scale back their distribution and dividend, and whereas ET made its distribution complete, KMI’s quarterly dividend is 55.88% of the place it was in This fall of 2015. This is not the case for EPD, as nothing has stood in the way in which of rising the distribution on an annual foundation for traders, and now EPD has reached the 25-year mark for consecutive annual distribution will increase.

Enterprise Merchandise Companions

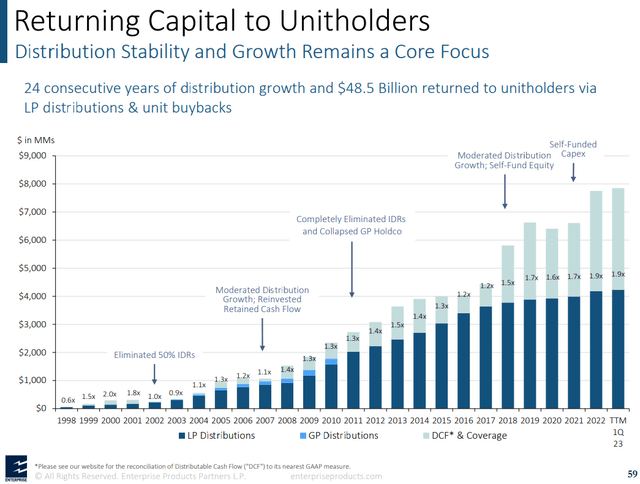

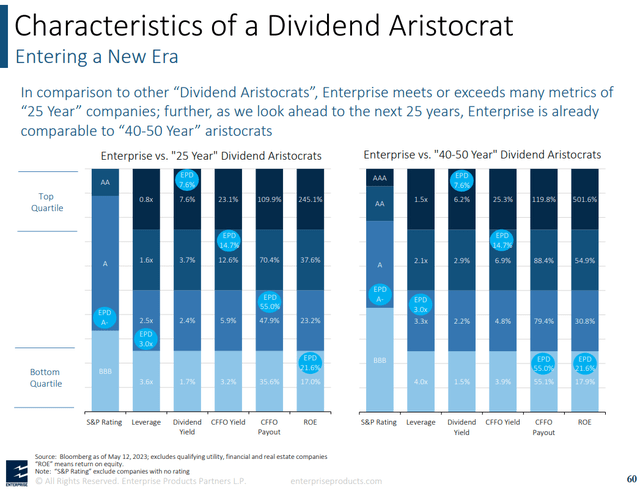

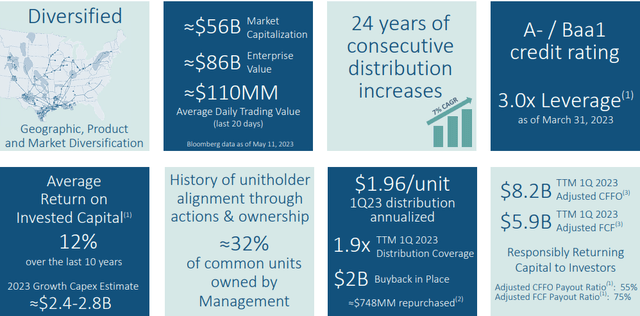

The slide above is from EPD’s investor deck which was revealed on 5/23/23. This slide will most probably be up to date to learn 25 consecutive years of distribution progress within the subsequent investor deck, which ought to be launched in August after earnings. I wished to include this slide into the article as a result of it demonstrates EPD’s proficiency in returning capital to unitholders. Whereas EPD isn’t an S&P 500 firm and can’t be named to the handy Dividend Aristocrat record, EPD has turn into an unofficial Dividend Aristocrat with a yield and distribution historical past that’s extra spectacular than most Dividend Aristocrats.

To turn into a Dividend Aristocrat, an organization have to be a member of the S&P 500 and have elevated their dividend funds consecutively for no less than 25 years. Corporations that accomplish this are held on a pedestal, so to talk, as a result of the accomplishment speaks volumes in regards to the firm’s sturdiness and talent to navigate enterprise environments over the long run. Whereas EPD is not an official Dividend Aristocrat, I consider its distribution is extra enticing than most Dividend Aristocrats. I’d put EPDs distribution up in opposition to any Dividend Aristocrat’s dividend profile any day of the week. I’m a shareholder of a number of Dividend Aristocrats, and whereas there are some Dividend Kings, reminiscent of The Coca-Cola Firm (KO), which I’ll by no means promote, there are solely two Dividend Aristocrats whom a case might be made for relating to their earnings profile, and people are Realty Revenue (O), and Federal Realty Belief (FRT).

Looking for Alpha

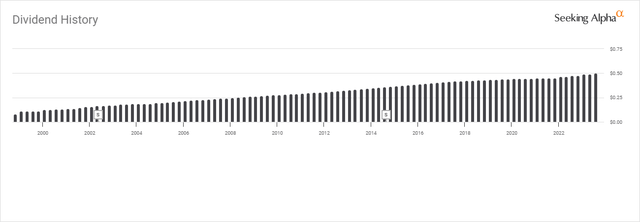

EPD began paying a distribution in This fall of 1998. Since they’ve undergone two inventory splits, the primary in 2002 and the second in 2014. For the reason that first distribution, EPD has paid 100 quarterly distributions, elevated the distribution for 25 consecutive years, and has turn into an unofficial Dividend Aristocrat. What’s extra spectacular is that EPD would not wait until the tip of the 12 months to supply the annual distribution enhance, typically, it offers quarterly will increase all year long. Since This fall of 1998, EPD has paid 100 quarterly distributions and offered traders with 78 quarterly distribution will increase. From This fall of 2004 to Q1 of 2020, EPD offered 62 consecutive distribution will increase. These stats are among the most compelling I’ve seen from an earnings funding perspective, because the string of quarterly distribution will increase has helped enhance EPD’s earnings technology a lot faster than different investments.

Dividend Channel

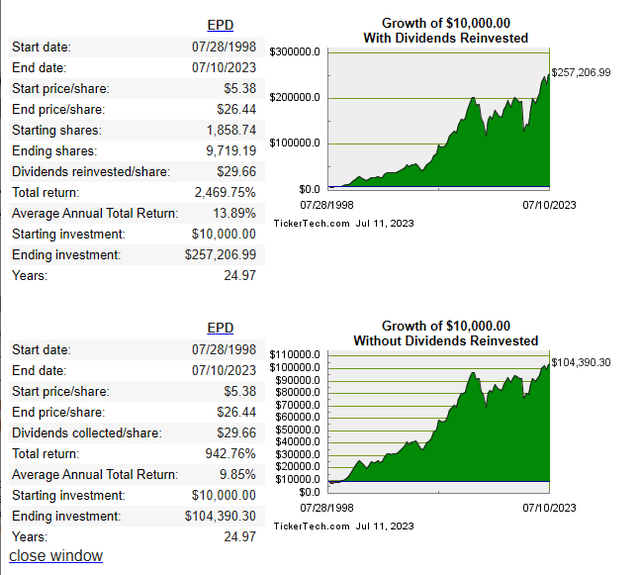

The facility of reinvesting dividends and distributions is immense, however from an earnings perspective, in the event you have been capable of reinvest the earnings over an extended time period, the quantity of earnings you’ll be able to generate sooner or later will turn into a lot bigger. When you had invested $10,000 in EPD at their IPO, you’d have bought 1,858.74 shares. The primary distribution for EPD was $0.08, so on an annualized foundation, EPD’s annual distribution would have been $0.32 per unit. The unique block of 1,858.74 shares would have produced $594.8 of annual distribution earnings. Over the following 25 years, EPD elevated its distribution on an annualized ahead foundation to $2. The distribution itself grew by $1.68 per unit or 525%. Over the course of the funding, in the event you had been taking the distributions as present earnings and never reinvesting them, you’d have collected $55,130.23 of earnings, and the models would now be producing $3,717.48 on an annual foundation.

The numbers turn into a lot totally different if the distributions had been reinvested over the previous 25 years. The identical $29.66 of distributions reinvested every quarter would have elevated the preliminary share rely by 7,860.45 models or 422.89%. The brand new unit complete can be 9,719.19, and between the brand new unit rely and the elevated distribution of $2, the present annualized distribution earnings can be $19,438.38. By reinvesting the distributions, you’d be producing a further $15,720.90 in distributions yearly, which is 422.89% greater than in the event you have been taking the earnings alongside the way in which. From an earnings perspective, EPD has been an impressive funding, and the numbers converse volumes about EPD’s distribution profile.

Enterprise Merchandise Companions

For earnings traders, the query turns into can EPD proceed its distribution will increase for many years into the longer term?

If I had a crystal ball and knew what was going to happen, I’d win Powerball each time I performed. No one can predict precisely what is going to occur 10 minutes from now, not to mention many years into the longer term. When I’m making funding choices, I’m working with the very best data I’ve at my disposal to type my funding thesis and decide. My feeling is that EPD might proceed rising its distribution properly into the longer term, and that is why I’m a unitholder. Once I say this, I accomplish that due to the knowledge that I’ve studied and shaped my funding thesis on.

There are a number of factors internally and externally that make me bullish on EPD as an earnings funding for the longer term. The 2 key metrics are distributable money circulate (DCF) and the DCF protection ratio. In Q1 2023, EPD’s DCF elevated 5.5% to $1.9 billion YoY. Its DCF protection ratio in Q1 2023 was 1.8x because it retained $863 million of DCF after its distributions have been paid. On a trailing twelve-month (TTM) foundation, EPD generated $7.85 billion in DCF with a 1.9x DCF protection ratio after its distributions have been paid. EPD has one of many largest footprints within the power infrastructure house with over 50,000 miles of pipeline, storage for liquids, pure gasoline processing crops, deepwater docks for exporting, and fractionators. When I’m investing in EPD, I’m investing in an organization that has bodily belongings which can be subsequent to unattainable for a brand new firm to compete in opposition to and displace as a consequence of regulatory necessities, environmental research, land necessities, capital wants, and the entire crimson tape. EPD has an extended monitor document of self-funding its CapEx and rising its DCF whereas offering a service that’s wanted by society. The query I have to reply is will oil & gasoline nonetheless be related a number of many years from now?

Enterprise Merchandise Companions

Based mostly on the knowledge I’ve at this time, oil & gasoline will nonetheless be wanted properly previous 2050. Whereas this might change as a consequence of technological breakthroughs, I’m basing my funding case on the knowledge the USA authorities offers by way of the Power Info Company (EIA) and the Worldwide Power Company (IEA) which is a global power authority. I’m additionally taking a look at information offered by BP and the newly shaped Power Institute, as I really feel BP places out the very best annual power studies within the business.

When you learn by way of the Power Institute Statistical Evaluate of World Power 2023, they’ve offered the entire important numbers. On a world scale, in 2022, oil manufacturing was 93.85 million barrels per day (Mbpd) which might be discovered on web page 15. The quantity of oil consumed every day in 2022 was 97.31 Mbpd, discovered on web page 20. In 2022 there was a mean deficit of -3.46 Mbpd between manufacturing and consumption. In 2022 the worldwide manufacturing of pure gasoline was 4.04 trillion cubic meters (Tcf) discovered on web page 30, and the worldwide consumption of pure gasoline was 3.94 TCF. The worldwide financial system utilized extra oil than was produced, and virtually all of the pure gasoline produced in 2022.

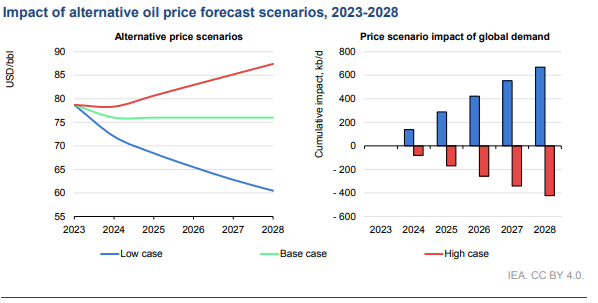

After understanding what is going on within the manufacturing and consumption of fossil fuels, I look to see what the EIA and the IEA are projecting out into the longer term for the oil & gasoline business. The newest oil 2023 evaluation and forecast to 2028 from the IEA, their reference case for oil stays above $75 via 2028. Of their low case, they see oil declining by way of 2028 however staying above $60, and on the excessive facet, oil is round $87.

Worldwide Power Company

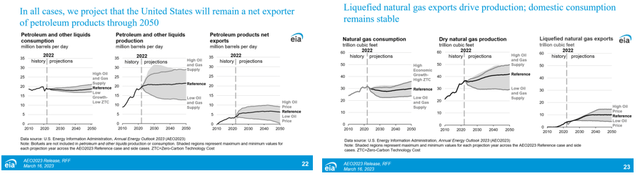

The EIA publishes two important studies: the Worldwide Power Outlook (revealed each two years) and the Annual Power Outlook. The Quick-Time period Power Outlook from the EIA is clearly indicating that U.S crude oil and liquid gas manufacturing, along with pure gasoline manufacturing, will enhance over the following two years. The reference case within the Annual Power Outlook from the EIA tasks that petroleum and different liquid manufacturing will barely enhance from now by way of 2050, and dry pure gasoline manufacturing will enhance by roughly 20% by way of 2050.

EIA

Once I put the items collectively, my assumption is that oil & gasoline will stay viable power sources for many years to return because the rising world inhabitants would require bigger quantities of power. Based mostly on this data, upstream corporations within the exploration and manufacturing section of the power business might want to transport oil & gasoline on a steady foundation, and if manufacturing grows as anticipated, then the transportation capability may also have to develop to satisfy demand. Whereas oil & gasoline might not be thrilling, the projections are that extra oil & gasoline shall be produced as many years cross. Once I tie all this collectively, it’s bullish for corporations reminiscent of EPD in my view.

Conclusion

EPD is now an unofficial Dividend Aristocrat as they’ve reached 25 years of annual distribution will increase. EPD’s distribution profile is extra thrilling than most Dividend Aristocrats, as its annualized distribution has grown by 525% ($1.68) since This fall of 1998. EPD has elevated its distribution 78 occasions over its 100 quarterly distributions paid. As an earnings funding, EPD generally is a cornerstone to any portfolio as its yield and distribution progress is difficult to match. EPD has a 1.9x DCF protection ratio, permitting it to organically develop its operations whereas rising distributions and shopping for again models. After trying on the power information accessible, it seems to be like oil & gasoline shall be right here for many years to return, and transportation capability might want to develop to satisfy the rising demand for power. I believe EPD is an undervalued gem, and earnings traders ought to contemplate researching this funding additional.

{kind=link}