Synthetic intelligence (AI) is likely one of the hottest industries for traders proper now. Semiconductor darling and information heart specialist Nvidia (NASDAQ: NVDA) is taken into account by many on Wall Road to be a profitable alternative for AI lovers.

With shares of Nvidia up over 170% up to now in 2024, some traders might imagine they’ve missed the boat.

Let’s check out what’s going on at Nvidia, and assess if now continues to be an inexpensive time to scoop up some shares.

Nvidia’s scorching begin to 2024

2023 marked a brand new age for the expertise business. Behemoths corresponding to Microsoft, Alphabet, and Amazon all made a sequence of splashy investments revolving round AI functions.

A few of the larger investments these tech giants made had been shopping for AI-powered semiconductor chips, in addition to ramping up information heart providers. Contemplating Nvidia has an estimated 80% share of the AI chip market, these strikes by huge tech undoubtedly served as an enormous increase to the corporate.

The robust momentum from final yr’s AI euphoria carried into 2024, and Nvidia traders have not stopped shopping for up the inventory. To place this into context, shares of Nvidia have elevated nearly 800% since January 2023.

This unprecedented run briefly catapulted Nvidia over Microsoft because the world’s Most worthy firm by market cap. Furthermore, as shares continued to eclipse new heights, Nvidia’s administration lastly determined to implement a 10-for-1 inventory cut up final month.

Nvidia is greater than only a chip alternative

What’s unimaginable is that a lot of the narrative surrounding Nvidia offers with the corporate’s chip enterprise. Certainly, its H100 and A100 graphics processing items (GPUs) are utilized by firms all all over the world — together with Meta Platforms and Tesla.

Furthermore, Nvidia is constant to steer the innovation entrance within the GPU realm with the introduction of its new Blackwell and Rubin chips.

With that stated, it is essential to grasp that Nvidia makes cash from different services as effectively. In reality, one in every of its lesser-known progress alternatives is outdoors of {hardware}.

Nvidia’s compute unified gadget structure (CUDA) software program platform is already proving to be a profitable enterprise. Basically, CUDA is a programming instrument that’s meant for use in parallel with Nvidia’s GPUs. So, in a way, the corporate is making an attempt to construct out an end-to-end AI ecosystem encompassing each {hardware} and software program.

One of many huge causes CUDA goes to be essential for Nvidia is because of competitors within the chip area. Corporations corresponding to AMD, Intel, and even Amazon and Meta are all engaged on competing GPUs to that of Nvidia.

Story continues

Though it is too early to get a way of how these competing merchandise will impression Nvidia, I feel it is moderately secure to say that the corporate will finally lose a few of its pricing energy within the chip area. Consequently, Nvidia’s revenue margins are more likely to take successful sooner or later sooner or later. Nevertheless, a few of this margin deterioration ought to be mitigated as long as CUDA continues to thrive. The reason being as a result of software program merchandise have a tendency to hold a lot increased margins than {hardware}.

Is now a superb time to spend money on Nvidia inventory?

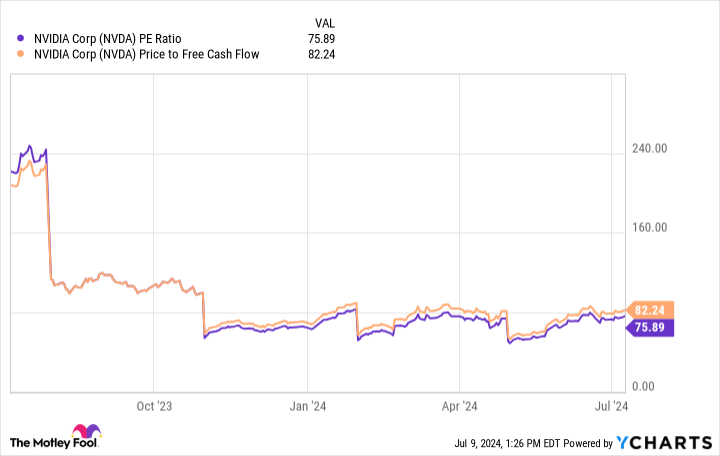

The chart under illustrates Nvidia’s price-to-earnings (P/E) and price-to-free-cash-flow (P/FCF) multiples during the last 12 months. Whereas a P/E of 75.9 and a P/FCF of 82.2 might look expensive, there are a few concepts to discover right here.

First, each Nvidia’s P/E and P/FCF multiples are decrease than they had been a yr in the past. In different phrases, regardless of the fast ascent of the inventory value, Nvidia’s earnings and money circulate are accelerating at a quicker price — due to this fact, Nvidia inventory is technically inexpensive at this time than it was 12 months in the past.

Furthermore, Nvidia’s commanding lead within the chip area and its under-the-radar software program providers ought to be analyzed additional. The corporate is an investor in Databricks, one of the vital beneficial AI start-ups on this planet. Nvidia can be an investor in Determine AI — a developer of humanoid robotics.

I don’t suppose that alternatives in robotics and AI software program are priced into Nvidia inventory but. I feel many of those functions are at present overshadowed by the efficiency of the chip enterprise, and plenty of traders are discounting the potential Nvidia has in different areas within the AI enviornment.

Lengthy-term traders have a chance to realize publicity to many alternative points of AI merely by means of Nvidia. Regardless of the meteoric rise in share value, the valuation evaluation above, in addition to a number of the different progress alternatives explored make a compelling case that Nvidia inventory is an effective purchase proper now and vital upside might very a lot be in retailer.

Do you have to make investments $1,000 in Nvidia proper now?

Before you purchase inventory in Nvidia, take into account this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they imagine are the 10 finest shares for traders to purchase now… and Nvidia wasn’t one in every of them. The ten shares that made the lower might produce monster returns within the coming years.

Think about when Nvidia made this listing on April 15, 2005… in case you invested $1,000 on the time of our suggestion, you’d have $791,929!*

Inventory Advisor gives traders with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of July 8, 2024

John Mackey, former CEO of Complete Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Randi Zuckerberg, a former director of market improvement and spokeswoman for Fb and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. Suzanne Frey, an government at Alphabet, is a member of The Motley Idiot’s board of administrators. Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Idiot has positions in and recommends Superior Micro Gadgets, Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Idiot recommends Intel and recommends the next choices: lengthy January 2025 $45 calls on Intel, lengthy January 2026 $395 calls on Microsoft, quick August 2024 $35 calls on Intel, and quick January 2026 $405 calls on Microsoft. The Motley Idiot has a disclosure coverage.

Is It Too Late to Purchase Nvidia Inventory After Its 10-for-1 Cut up? was initially revealed by The Motley Idiot