Dmitry Vinogradov

Funding Thesis

In Q3 FY’23, I advocated closely to allocating to the essential supplies sector because it introduced with the very best development prospects albeit on the smallest weighting of the S&P 500 Index sectors [avid readers of this channel will remember this]. This was nonetheless true on the finish of Q1 FY’24 (Determine 1). I proceed to see worth on this area on a worth/worth foundation, which introduced me to find out the funding prospects of Hawkins, Inc.’s (NASDAQ:HWKN).

HWKN is a number one specialty chemical and components firm, offering options to industrial, water therapy, and well being and diet sectors. It operates ~60 amenities in 26 states. The corporate’s operations are segmented into three major divisions:

Industrial: Focuses on supplying industrial chemical compounds, together with acids, alkalis, and food-grade merchandise. Water Therapy: Focuses on water therapy chemical compounds and companies. Well being and Vitamin: Gives dietary components and health-related chemical merchandise.

What’s piqued my curiosity in HWKN is its prioritization of buying water utility belongings, that are a degree of differentiation with hard-to-replicate enterprise benefits for my part. Because it started the acquisition path on this section in FY’23, ROICs are ~200-300bps greater and administration has a brand new runway to deploy capital in the direction of. It’s presently reinvesting ~65% of NOPAT each 12 months.

Whole gross sales have been ~$919mm in FY’24, down 200bps from a excessive base in ’23, however gross revenue was +17% to $194mm ($9.20/share) – partly as a result of LIFO decreases – with ~26% in earnings to $0.73/share.

That is however among the proof corroborating a purchase on this identify, together with 1) excessive and rising ROICs on secure capital base [ROICs are +300bps to ~16% in FY’24], 2) administration’s reinvestment alternatives to deploy capital at these charges, and three) valuations supportive ~$109/share on multiples of capital however ~$160/share on NOPAT multiples indicating marginal threat of error is low.

Web-net, charge purchase.

Determine 1. Retrieved from writer’s analyses round Might FY’24.

Creator’s estimates, Bloomberg, In search of Alpha

Why HWKN is a high-quality enterprise

The corporate was based in 1938 and produced ~$920mm in FY’24 gross sales with simply 970 staff [~$947k in revenue/employee]. It booked internet revenue per worker of ~$81K in FY’24, fourth highest within the commodity chemical compounds business [behind (CBT), (LYB), and (MEOH) respectively – MEOH did >$115K profit/employee, so the gap isn’t wide either]. It isn’t simply the return on expertise driving the enterprise – capital productiveness + profitability is equally excessive, because of distinctive drivers. My view is we will anticipate ~50% cumulative earnings energy by FY’26E (Determine 3).

I begin with the corporate’s enterprise drivers:

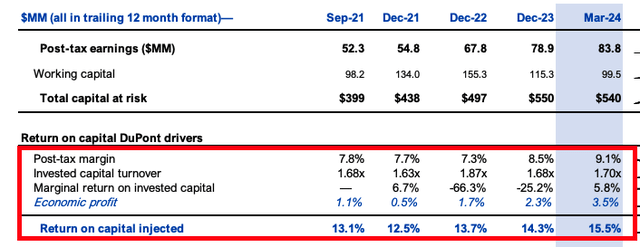

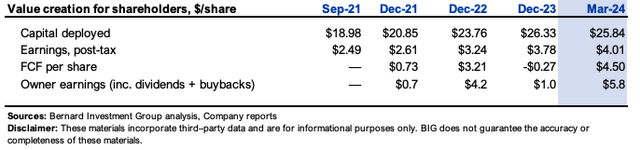

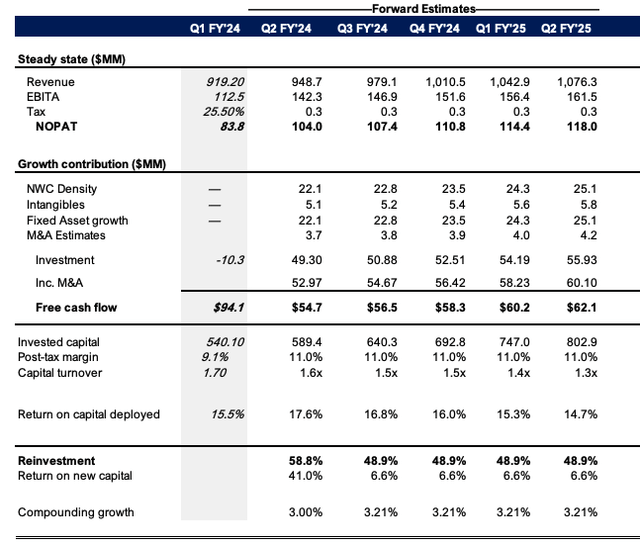

HWKN is incomes extra on the expansion + legacy capital that is been put into the enterprise + invested since FY’21 – ROICs are +350bps to fifteen.5% in FY’24 as 1) NOPAT margins have expanded ~120bps, and a pair of) capital turns remained at ~1.7x. Particularly, its FY’23-’24 acquisitions – EcoTech, Water Options Limitless, Miami Merchandise & Chemical + Industrial Analysis Corp – have added ~$70mm in incremental gross sales. Critically, I get to ~14% ROICs by FY’25 pushed by 3.2% compounding gross sales development, ~15% pre-tax margin and capital deployment charge of $0.48-$0.50 per new greenback of revenues [see: Appendix 1]. These economics see HWKN throw off ~$550mm in FCF [+$200mm since FY’21] used for 1) development reinvestment, 2) dividends, and three) buybacks. Since FY’21, administration reinvested ~$6.85/share into the enterprise [predominantly acquisitions] and grew NOPAT $4.50/share – 22% marginal return on capital (Determine 3). The trailing proprietor earnings yield (i.e., FCF with all dividends + buybacks paid up) is ~6% as I write.

Determine 2.

Firm filings

Determine 3.

Firm filings

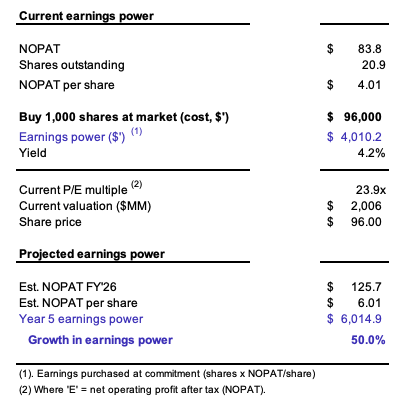

My view is that based mostly on 1) gross sales development estimates, 2) charge of capital deployment [reinvestment rate is conservative at ~13% of NOPAT] and three) ROICs of ~19%, this might see us acquire ~50% cumulative development in earnings energy to acquire ~$6.00 NOPAT/share by FY’26E (Determine 4). I will run the situation with proudly owning 1,000 HWKN shares at market at present with value = ~$96,000. For this, we acquire ~$4 NOPAT/share for an earnings energy of ~$4,000. By FY’26E, if the enterprise grows on the assumptions above, this produces ~$6,000 in earnings energy [~14% CAGR, ahead of our 12% required rate of return].

Determine 4.

Creator’s estimates [see: Appendix 1]

Valuations supported by strong economics

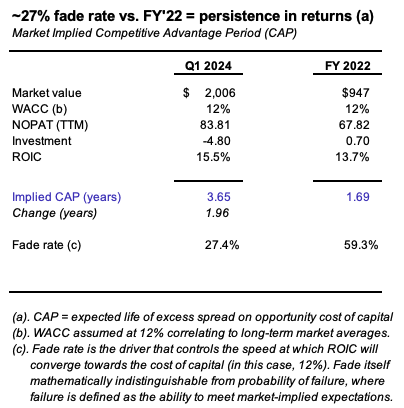

The combo of 1) greater and rising ROICs, 2) longer reinvestment runway to deploy capital [esp. within the water utilities sector] and three) +10% earnings development projected to FY’26E my view is the corporate’s aggressive benefit interval (“CAP”) has prolonged to >3.6 years and the fade charge on this has decreased to ~27% vs. 60% in FY’22 [note: fade is analogous to the probability of failure]. The <30% fade charge signifies persistence in its current enterprise returns; I’m constructive on this (Determine 5.a.).

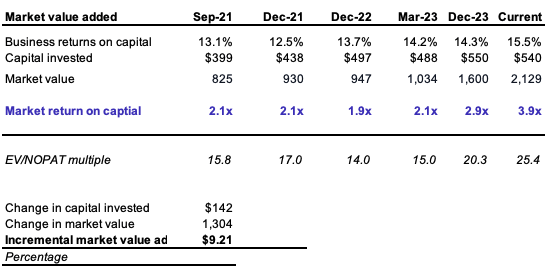

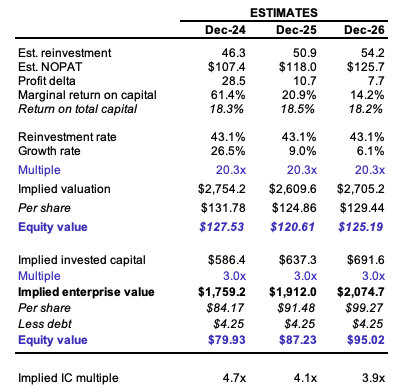

Multiples on capital + earnings have stretched greater since ’21 – (i) EV/IC is +1.8x and (ii) ~EV/NOPAT is +9.5x, valuing the present enterprise operations at 3.9x and 25x respectively (Determine 5). The enlargement is well-supported by the financial knowledge. The speed of capital deployment + subsequent returns justify ~$127/share at present, even at a decreased 20x NOPAT a number of [reminder from above: it trades at ~25x today]. I will run with these conservative assumptions for now, though I am acutely conscious that the market could proceed paying extra (which is bullish to the thesis).

Determine 5.

Firm filings, writer

Determine 5.a.

Firm filings, writer

Valuation insights

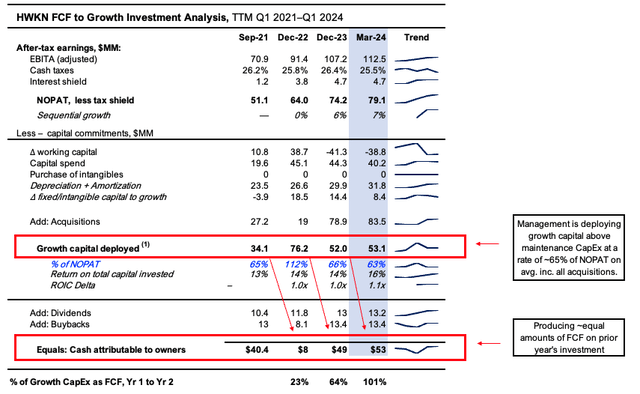

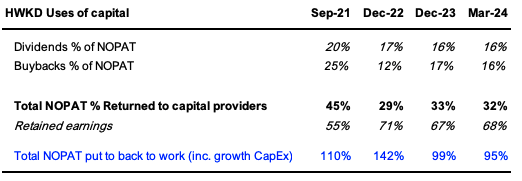

The +1.8x development in EV/IC a number of from FY’21-’24 outcomes from administration’s financial efficiency – The reinvestment runway is apparent with 1) +$30-80mm in development CapEx allotted every 12 months [growth investment = all CapEx above the maintenance capital charge, which is approximated at depreciation + amortization], and a pair of) the >12% ROICs which elevated by +300bps, as talked about earlier. Administration is thus aggressively deploying funds on this enterprise, straight reinvesting ~65% NOPAT again into operations on avg. [inc. all acquisitions] and returning ~30% to shareholders [down from 45% in FY’21 as evidence of the greater business opportunities]. The cut up is presently ~16%/16% dividends + buybacks, respectively. Thoughts you, it’s now rolling off ~100% money return on every year’s development investments [using Yr2 FCF / Yr1 growth CapEx = cash ROI as a crude measure of this] – (observe, see: Determine 6 and Determine 7).

Determine 6.

Firm filings, writer

Determine 7.

Firm filings, writer

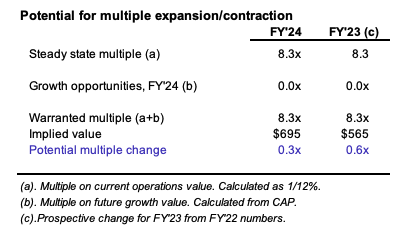

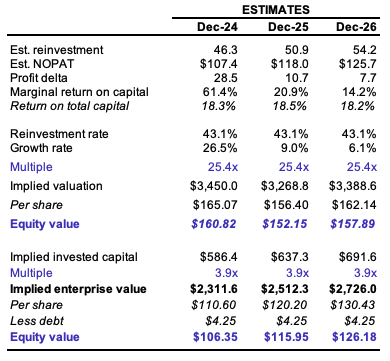

The present enterprise is valued ~25x NOPAT, however my view is the market may worth its future investments at ~20x which nonetheless implies ~$127 market worth at present – Attention-grabbing dilemma right here in that 20.3x NOPAT is ~20% contraction from the present c.25x a number of, however implies the inventory is price 4.7x capital – a 20% enlargement. My tackle that is 1) the market values its acquisitions extremely, and extra critically 2) HWKN’s earnings have gotten extra beneficial with each greenback administration throws again into the enterprise. Thus – (i) administration ought to get excessive marks for any additional reductions in dividend/buyback payout ratios, and (ii) any selections to re-route that capital into operations ought to be seen very favourably. Worth of HWKN’s future enterprise could possibly be ~20x NOPAT if multiples contract ~0.3x from present costs. The danger of contraction is decrease [fade rate ~27% vs. ~60% in FY’22], however the market could have HWKN operating a bit too sizzling anyway, as talked about. Presuming it does worth all future earnings this fashion, my numbers get to +$26mm in NOPAT from Q1 ’24 (TTM values – see: Appendix 1), producing $110mm in post-tax earnings for FY’24. A 20.3x a number of on this means ~$524mm or $25/share in further market worth (20.3 x $26 = $524mm).

Determine 8.

Creator’s estimates

Determine 9. The worth of earnings is getting extra beneficial with every $1 of incremental capital that administration employs into the enterprise.

Creator’s estimates

Determine 10. Valuation ranges if traders proceed valuing HWKN at ~25x NOPAT.

Creator estimates

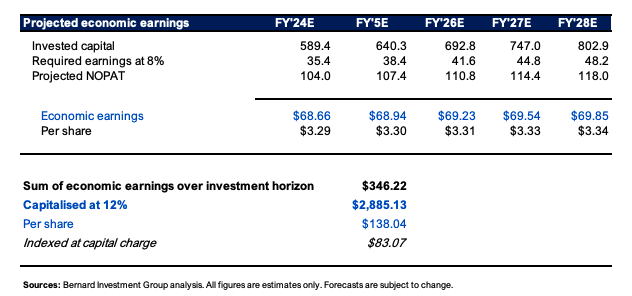

Lastly, discounting the estimated surplus money flows above similarly-risked investments at a 12% hurdle charge implies the inventory is price ~$138/share at present within the base case. Thoughts you, this case is extremely conservative with (a) 3.2% compounding gross sales development, (b) ~15% EBIT margins, and (c) capital deployment charge of ~50% of NOPAT – under the present figures. I’m thus projecting 1) decrease multiples, 2) tighter reinvestment charge, 3) a fade in ROICs to 14% by FY’25, and three) a excessive low cost charge and nonetheless exhibiting asymmetrical upside reward on this case.

Determine 11. Extra earnings above 6% investment-grade corporates’ beginning yields, discounted at 12% hurdle charge.

Creator’s estimates

Dangers

Draw back dangers to the thesis embody 1) EBIT margins contracting <15%, 2) valuations compressing <20x NOPAT, 3) administration making poor acquisition decisions [thus spoiling the ROIC profile] and 4) the inflation/charges axis that continues to plague fairness markets. Additional unhealthy inflation knowledge is a serious draw back threat.

Buyers should perceive these dangers in full earlier than continuing any additional.

In brief

HWKN presents with distinctive economics that warrant a purchase ranking as a result of 1) excessive and increasing ROICs, 2) profitable acquisitions now pulling their financial weight, 3) elevated reinvestment runway to deploy funds again into the enterprise better off vs. market returns, and 4) valuations supportive regardless of extremely conservative assumptions.

For example, I’ve 1) decreased implied a number of ~20%, 2) contracted implied capital deployment charges, 3) light the ROICs to 14%, and 4) utilized heavy discounting to projected money flows, and nonetheless, I imagine the inventory is price ~$127-$138/share at present. Price purchase.

Appendix 1.

Creator’s estimates

{kind=link}