Sundry Pictures

As we come up on Atlassian Company’s (NASDAQ:TEAM) This fall and Annual Report 2024 on August 1, 2024, I feel an replace to my February 10 thesis is so as. On the time, I really useful a Promote score based mostly on the incontrovertible fact that the corporate had no working leverage and that effectivity metrics corresponding to ROE, ROTC, and ROA had been all struggling to get above breakeven. What added gasoline to the bearish hearth was that the corporate was regularly guiding for weak cloud revenues. Q3 2024 outcomes had been reported since then, and now that we’re on the verge of taking a look at full-year and This fall outcomes, we must always check out how these metrics have performed out and are anticipated to play out when earnings are introduced subsequent month.

On the one hand, key profitability metrics have been bettering quarter over quarter; on the opposite, we’d have to see some stability and sustainability in these enhancements to immediate a score improve to a Maintain. I’m nonetheless not ruling out a Purchase name even additional down the highway if I really feel the valuation is justified.

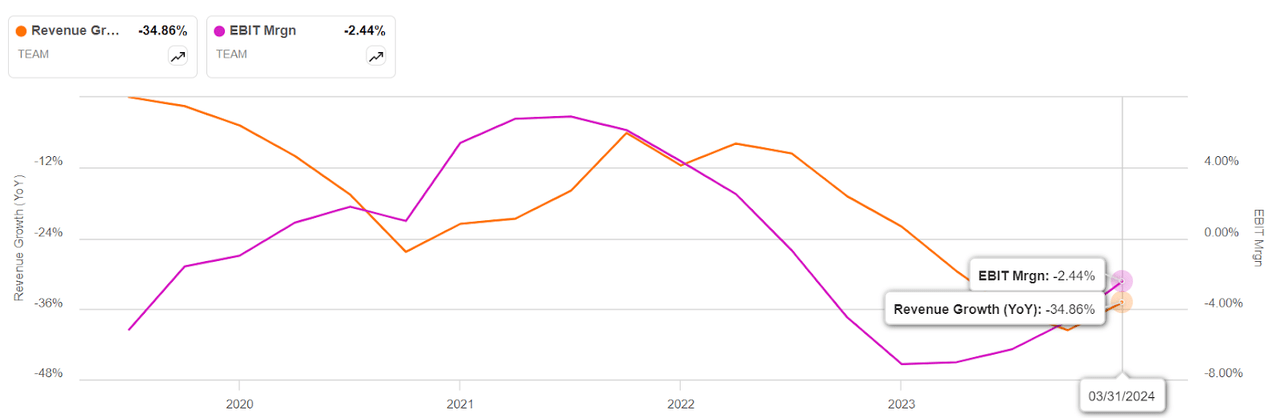

Income and Profitability Developments Since Q2 2024

The one factor that was constructive was whole income development, even after I wrote my bearish thesis. Revenues did weaken in Q3 on a YoY foundation, however solely marginally. TEAM continues to be rising its quarterly revenues close to the 30% degree year-over-year. The issue, as we noticed in my earlier article, is one in all working leverage, and that development repeated itself in Q3, as I think it’ll in This fall as effectively. Though the numbers appear to be bettering quarter over quarter, I’d wish to see much more consistency. That’s the one approach issues can enhance in the long run.

SA

That being stated, there’s actually a constructive ingredient that got here out of that: Q3 confirmed a constructive GAAP working earnings, versus a 1.9% working loss in Q1 and a extra worrisome 4.6% loss in Q2, which translated to a internet earnings margin of simply over 1%. Not fairly what bullish traders may need anticipated, and I feel it was extra of a brief suppression of each SG&A and R&D spending, each of which TEAM can not afford to ease up on to any vital diploma. It’s going to hit income development badly in the event that they do. Nonetheless, Q3 noticed a bit of wiggle room there – nearly sufficient to permit the corporate to submit constructive working and internet incomes, with a GAAP EPS of $0.05.

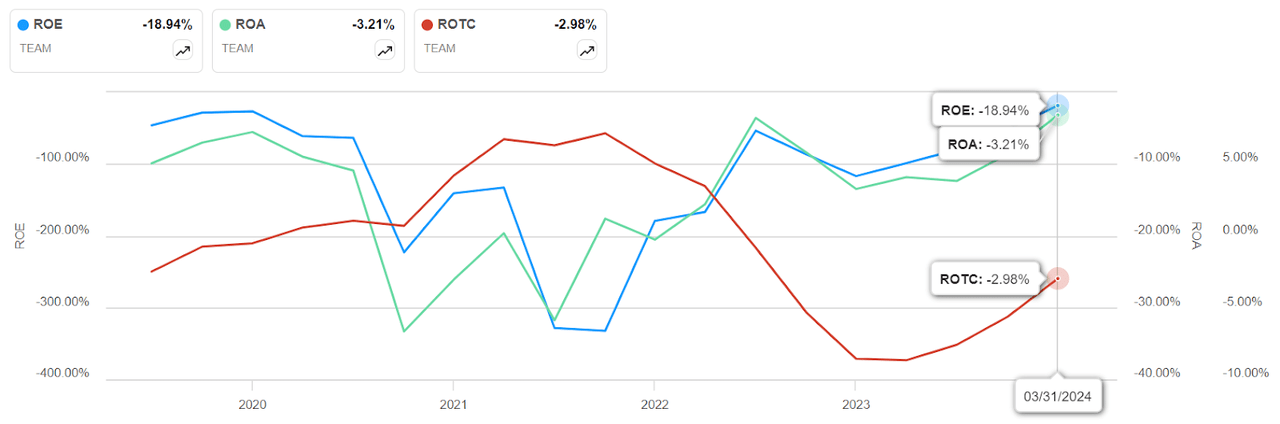

On account of Q3’s considerably constructive outcomes and the truth that its profitability metrics have incrementally improved over the previous few quarters, TEAM’s effectivity metrics have additionally improved within the TTM. ROE, ROTC, and ROA, which had been at -52%, -5.6%, and -8.6%, respectively on the finish of 2023 at the moment are considerably nearer to zero, at -19%, -3%, and -3.2%, respectively, on a TTM foundation as I write this. I think there shall be a bit of extra monetary engineering within the works to get these numbers as much as breakeven on the finish of This fall.

SA

Throughout that point, nonetheless, the inventory has continued to slip, declining almost 20% because the starting of February, proper after Q2 earnings had been introduced. Q3 noticed a extra precipitous drop, but it surely now seems like investor sentiment is rotating into constructive territory, with the fill up 12% within the final month.

Reassessing (Or Reiterating?) My Bearish Thesis

Does that imply my bearish thesis is now invalid? I’m undecided that it’s. Once I take a look at valuation modifications between at times, I nonetheless see indicators of weak spot. This enterprise will not be at the moment value 63x ahead GAAP earnings, even when it’s down from the +80x degree that it was almost two quarters in the past. In my February article, I stated that if “you’re keen to proceed holding on to a dangerous funding, you might simply be caught with it till the corporate turns worthwhile on a constant foundation and begins exhibiting constructive returns on the property it possesses, the capital it deploys, and the fairness that’s reinvested into the enterprise. And that could possibly be a really very long time.”

Why do I nonetheless suppose so? My largest purpose is that the enhancements in profitability can solely be thought-about sustainable in the event that they present constructive tendencies over a number of quarters. Whereas I’ll admit that the corporate may be on the verge of turning persistently GAAP-profitable on the working and internet ranges, the present excessive rate of interest surroundings would possibly make it exhausting for subscriptions to continue to grow on the present tempo. Primarily, that’s what’s driving the borderline profitability at this level, and with the corporate guiding for a 7% working loss margin in This fall, that retains the timeline to constant profitability pretty distant.

I’ll say it as soon as once more – income development has not been an issue over the previous few quarters. The problem has at all times been about profitability, and the necessity to more and more and disproportionately spend extra to make extra. As I stated in my earlier article, cost-cutting and operational efficiencies aren’t the reply to this bigger drawback.

This isn’t to say that I don’t perceive the challenges, after all. Competitors is hard on this house, and though a lot of Atlassian’s merchandise dominate their segments, development is pricey. Nevertheless, though I’ll grant that This fall steerage was a bit of stronger than what we noticed by means of the primary half of the 12 months, a 32% cloud income development fee and 40% to 42% knowledge middle income development vary may not resolve that greater drawback. I feel we’ll proceed to see excessive SG&A in addition to R&D spends within the vary of 30s and excessive 40s as a share of revenues.

What are the Upside Dangers to a Bearish TEAM Thesis?

The apparent threat is that This fall will present improved profitability and FY25 will proceed that upward development. If that occurs, valuation ranges are naturally going to return down nearer to sensible ranges. At that time, I’d be more than pleased to fee this a Maintain or perhaps a Purchase. Even a few extra quarters exhibiting improved profitability and continued income development within the 30% vary can be constructive sufficient to sign a Maintain. I consider administration guided fairly conservatively for This fall, projecting a 27% development fee on the midpoint of $1.120 billion and $1.135 billion, over $885.6 million within the year-ago interval, and I think that stems from an extra downsizing of SG&A and R&D spending. However, if that concentrate on is achieved, I feel we’ll see yet another quarter of GAAP profitability. It may not be sufficient to interrupt my thesis down utterly, however I’ll concede that my bearish views are beginning to present indicators of degradation.

One query that traders can have on the tops of their minds might be in regards to the CEO transition. After 23+ years co-helming Atlassian with co-founder and co-CEO Mike Cannon-Brookes, co-CEO Scott Farquhar will relinquish his present position on the finish of subsequent month. Will this influence the enterprise in any detrimental or constructive approach? My opinion is that it gained’t both approach, as a result of that is very doubtless a well-thought-out plan that may place the reins firmly in Cannon-Brookes’ fingers however nonetheless see Farquhar play an energetic advisory position, if not an govt one.

Some Closing Ideas

Lastly, I’d wish to make clear that my bearish stance on the inventory doesn’t imply I’m bearish on the corporate or its enterprise mannequin. Atlassian has an extended development runway forward of it, and I consider that despite the fact that it’ll take a number of quarters to develop into sustainably worthwhile, the inventory received forward of itself far too early within the sport.

And it is a drawback I see with lots of fast-growing tech corporations, together with, dare I say, Nvidia (NVDA), on which I’m nonetheless very a lot bullish. That bullishness is contingent on a number of issues, together with the best way I see the timeline within the AI GPU panorama progressively evolving to permit extra gamers to take up robust positions and vital market share, particularly Superior Micro Units (AMD), an organization I wrote about simply final week.

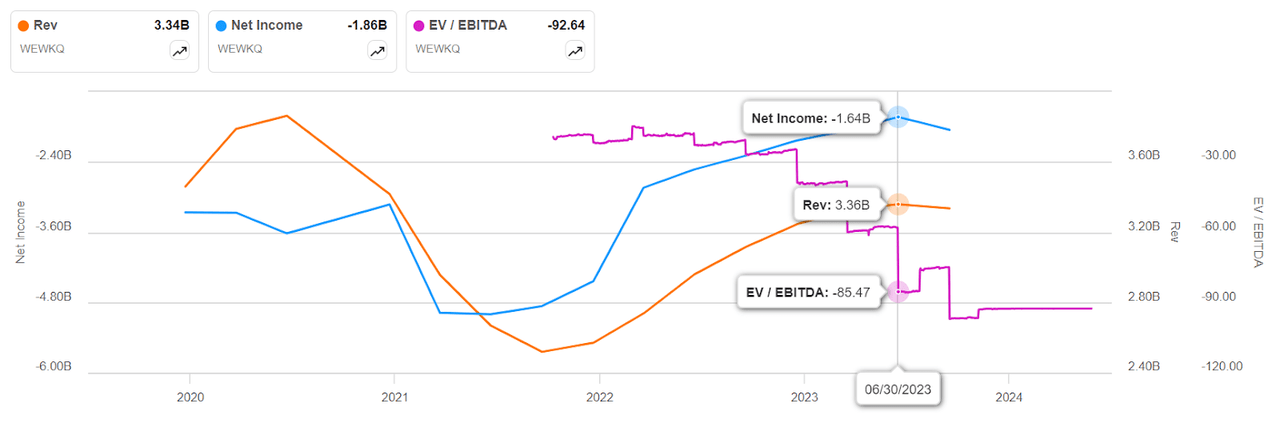

Many different fast-growers, sadly, have seen their valuations skyrocket on market optimism, solely to return crashing down as a result of they had been valued too extremely to start with. Simply take a look at what occurred with WeWork (OTC:WEWKQ). Its revenues had been within the billions of {dollars} a 12 months, however as a result of it couldn’t develop into sustainably worthwhile, it spiraled rapidly into chapter 11. In fact, its topline development wasn’t as robust as what now we have with TEAM, and that merely highlights the significance of constant to develop revenues alongside a targeted effort to develop into persistently worthwhile in the long run.

SA

I don’t see such an issue with TEAM by any stretch of the creativeness, so I’m positive I’ll ultimately develop into bullish on the inventory. Not proper now, although, and never on the present valuation with out the promise of constant earnings being generated quarter after quarter. So far as I can see, TEAM is doing it proper, rising its revenues by spending extra, however well-aware of the necessity to obtain the suitable stability of development, profitability, returns-based effectivity, and valuation to develop into a transparent Purchase for many traders. Whereas it’s nonetheless a Promote at this time limit, I do see myself upgrading this to a Maintain over the following couple of quarters. I’m simply ready for the suitable numbers to be reported and the suitable degree of metrics that I count on to be assured with that decision.

{kind=link}