Enbridge (NYSE: ENB) will not be an thrilling firm, however that is really one of many largest sights right here. That and an ultra-high dividend yield of round 7.4%. However to essentially recognize why you will be glad you got this inventory in a number of years, you’ll want to take a deeper dive into its enterprise and the way it returns worth to buyers over time.

Enbridge is greater than a midstream big

The vitality sector is thought for being unstable, however not each firm within the trade deserves that label. Upstream (drilling) and downstream (refining and chemical substances) companies are sometimes fairly unstable, however midstream companies like Enbridge often aren’t. That is as a result of midstream corporations personal the vitality infrastructure (like pipelines) that connects the upstream to the downstream, and the remainder of the world, and so they largely cost charges for using their belongings.

Enbridge is, principally, a toll taker. And since oil and pure gasoline are very important to the world functioning easily, demand tends to stay sturdy even when vitality costs are weak. Oil pipelines account for round 50% of earnings earlier than curiosity, taxes, depreciation, and amortization (EBITDA) whereas pure gasoline pipelines make up roughly 25%. Which is the place the subsequent attention-grabbing truth about Enbridge arises.

The remainder of the vitality big’s enterprise comes from regulated pure gasoline utilities (22% of EBITDA) and renewable energy investments (3%). Pure gasoline is cleaner-burning than coal or oil and is seen as a transition gas. Enbridge not too long ago agreed to purchase three pure gasoline utilities from Dominion Vitality, which elevated its publicity to this vitality area of interest from 12% as much as above 22%. Regulated utility belongings are given a monopoly within the areas they serve in trade for being required to get charges and funding plans authorized by the federal government. That tends to result in gradual and regular development over time. Briefly, Enbridge’s enterprise is much more dependable because of this funding.

Then there’s the renewable energy enterprise, which is pretty small relative to the remainder of the corporate. However then clear vitality continues to be a comparatively small piece of the worldwide vitality pie, too. The truth that Enbridge is increasing into the area is principally an try to make use of its carbon gas earnings to vary together with the world as clear vitality turns into extra necessary over time. It represents a hedge, of types, for buyers who aren’t prepared to leap into renewable energy however acknowledge its rising function on the planet.

What can buyers count on from Enbridge?

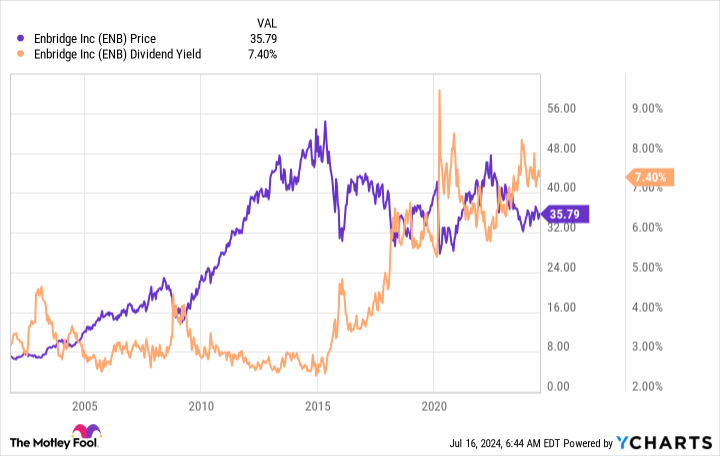

So Enbridge is a boring midstream firm that is slowly altering its enterprise in a cleaner course. That is not precisely an thrilling story till you take into accounts the massive 7.4% dividend yield. Most buyers count on the inventory market as an entire to supply returns of roughly 10% a 12 months, so Enbridge’s dividend alone will get you roughly three-quarters of the way in which there.

Story continues

That dividend, in the meantime, is backed by an investment-grade-rated steadiness sheet. And the distributable-cash-flow payout ratio is correct in the midst of administration’s 60%-to-70% goal vary. The dividend has additionally been elevated yearly for 29 consecutive years. This can be a dependable dividend inventory and there is no motive to consider that the dividend is in danger. The truth is, it appears extremely probably that gradual and regular dividend development within the low single digits is an affordable expectation.

So, if the dividend grows roughly according to inflation, at about 3%, the full return buyers can count on might be about 10%, including the present 7%-plus yield to the dividend improve of round 3%. Usually, shares rise together with their dividends over time to maintain the yield fixed, so market-like returns from this high-yield inventory is not an unrealistic expectation. That is arduous to complain about, notably in the event you reinvest your dividends, which permits them to compound over time.

The bottom case for Enbridge is nice

It appears probably that Enbridge can handle to only plod alongside doing what it’s doing. That will probably be sufficient to supply stable returns to buyers, as famous above. However what’s attention-grabbing right here is that Enbridge’s dividend yield is traditionally excessive at the moment. So it really seems like it might be buying and selling at a depressed value.

It’s solely doable that this example does not change and the yield has merely risen into a brand new vary to replicate Enbridge’s enterprise because it stands at the moment. Nevertheless, if Wall Road instantly turns into extra within the firm, buyers who purchase at the moment will get a lift from elevated demand for the shares. The bottom case is for Enbridge’s boring enterprise to supply roughly market-like returns whereas the upside might be a lot greater. That looks as if a lovely threat/reward steadiness that you’re going to be sorry you missed out on in the event you do not bounce aboard quickly.

Do you have to make investments $1,000 in Enbridge proper now?

Before you purchase inventory in Enbridge, think about this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they consider are the 10 finest shares for buyers to purchase now… and Enbridge wasn’t certainly one of them. The ten shares that made the lower may produce monster returns within the coming years.

Contemplate when Nvidia made this checklist on April 15, 2005… in the event you invested $1,000 on the time of our suggestion, you’d have $722,626!*

Inventory Advisor offers buyers with an easy-to-follow blueprint for achievement, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of July 15, 2024

Reuben Gregg Brewer has positions in Dominion Vitality and Enbridge. The Motley Idiot has positions in and recommends Enbridge. The Motley Idiot recommends Dominion Vitality. The Motley Idiot has a disclosure coverage.

A Few Years From Now, You may Want You’d Purchased This Undervalued Excessive-Yield Inventory was initially printed by The Motley Idiot