Worawee Meepian

This 12 months’s rally has largely been in regards to the AI surge, however after we take a step again, the guts of AI is automation, and automation has been vibrant in lots of industries for years.

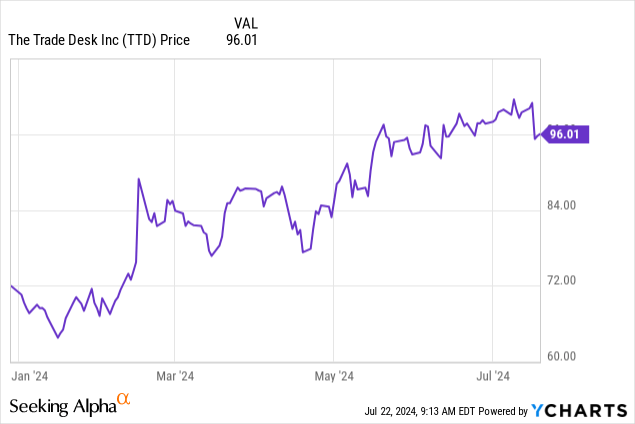

Championing automation and effectivity within the gigantic promoting business has been the bread and butter of The Commerce Desk (NASDAQ:TTD) since its inception in 2009, and this 12 months, the inventory is rallying sharply (up almost 40% 12 months up to now) on a driver that has little to do with AI: the rise of the linked TV. Progress is accelerating, pumping an increasing number of worth into The Commerce Desk’s inventory.

Typically, I’d method these richly valued firms with a big measure of warning, and I’d err on the facet of promoting these off to spend money on extra value-oriented names. However for my part, The Commerce Desk has that “particular sauce” with multi-year progress drivers to justify its premium valuation regardless of the rally it has beneath its belt.

I’m assigning a purchase ranking to this phenomenal progress inventory. In my opinion, listed below are the core causes to be bullish on The Commerce Desk:

Huge TAM – There are few industries on this planet which can be as profitable and world as promoting. The Commerce Desk estimates that its addressable market tallies as much as a staggering $1 trillion. Progress at scale, powered by linked TV – What’s a TV as of late if it may well’t entry web purposes? Machine makers equivalent to Roku (ROKU) have been emphasizing advertising-supported options on their rising put in base of customers. Subscription firms are additionally turning to promoting to broaden their income streams. Few web content material networks are working a subscription-only or ad-only enterprise mannequin; now, it’s much more widespread for media firms to supply each plans, to attraction to customers at completely different value factors. As firms like Netflix (NFLX) proceed to construct out their promoting companies, business contributors like The Commerce Desk will proceed to profit. Business too advanced to handle with out know-how and automation – Maybe the one clear examples of “analog”, or non-automated, advert gross sales are bigger spot offers just like the Tremendous Bowl. However in an business with numerous advertisers (purchase facet, manufacturers each giant and small), publishers (the promote facet, starting from giant media networks to unbiased blogs), advert exchanges, and middlemen like promoting companies, it’s not possible now to think about the circulation of the ad-buying course of with out know-how like The Commerce Desk, guaranteeing its longevity.

In my opinion, The Commerce Desk’s progress acceleration this 12 months is a testomony to the largesse of its market, and helps to justify why near-term multiples are so elevated. And it’s not only a “progress in any respect prices” story, both: the corporate’s income (it prides itself on having been worthwhile since 2013, really a rarity for fast-growing tech shares) are rising sooner than the highest line. Regardless of the robust YTD rally, I’d encourage traders to maintain holding on for extra upside forward.

Accelerating progress rarity in firms of this scale

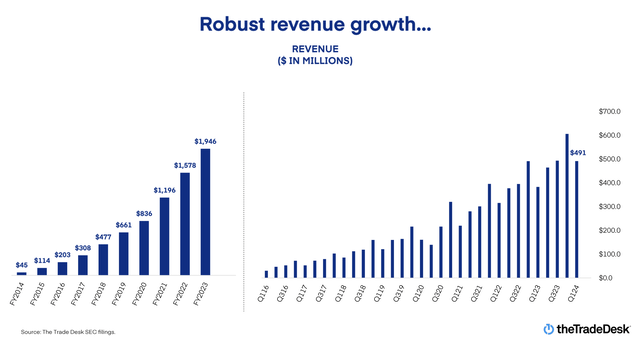

Typical tech firms comply with a predictable progress sample: they burst with explosive progress charges firstly of their lives as they seize extra share of their market, after which ultimately they turn into a sufferer of their very own scale and steadily decelerate to extra unimpressive, secure progress charges. However regardless of hitting over $2 billion in annualized income run charges, The Commerce Desk is experiencing important acceleration. Check out its quarterly income, trended over time:

The Commerce Desk trended income (The Commerce Desk Q1 earnings deck)

In its most up-to-date quarter, Q1, The Commerce Desk achieved 28% y/y income progress to $491 million, blasting previous Wall Avenue’s expectations of $480.5 million (+26% y/y). This accelerated 5 factors versus 23% full-year progress in FY23.

There are each secular and company-specific deal successes right here, and we’ll begin with the broader secular themes. The largest driver that we talked about upfront is powerful progress in linked TV. Progress on this sphere is coming from all angles: shoppers are consuming extra web TV content material than conventional or “linear” TV, machine makers like Roku are placing out linked TVs at accessible costs for all audiences, and advertisers are additionally shifting their spend away from conventional TV and into the web, with their advert {dollars} following the place the viewers’ eyeballs are going.

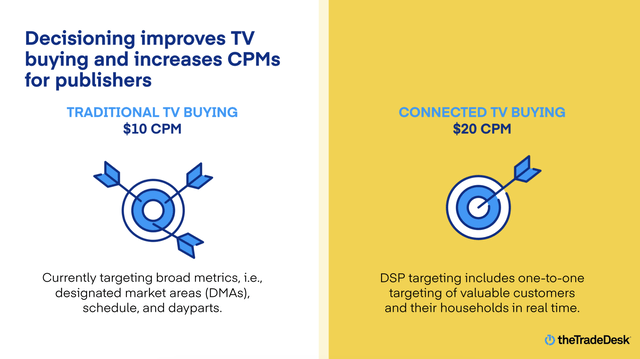

Nevertheless it’s not nearly extra leisure being consumed on-line versus on broadcast, both. Linked TV has the benefit of having the ability to goal customers extra particularly (versus conventional promoting being extra of a “spray and pray” method), which is the place publishers of digital content material have a bonus over linear or broadcast. In response to the Commerce Desk, the CPM (price per mille, an promoting time period for the price of reaching one thousand distinctive impressions or views) of conventional TV spend is $10, whereas linked CPM is $20. Clearly, content material publishers are going to concentrate on promoting stock the place CPM is highest. And on the advertiser (demand) facet, extra knowledge and analytics can be found for the success and outcomes of web promoting, typically greater than justifying the upper price.

CPMs for conventional vs. linked advertisements (The Commerce Desk Q1 earnings deck)

Past these secular tailwinds, The Commerce Desk has additionally achieved numerous enviable, high-profile offers. Specifically, the corporate inked a take care of NBCUniversal to make advert stock for the 2024 Paris Summer season Olympics out there by way of The Commerce Desk. In response to the corporate, it’s the primary time that the Olympics’ advert segments are being offered programmatically, marking an vital shift for marquee and legacy occasions away from analog shopping for and into automated shopping for. The corporate additionally inked related offers to make extra advert stock from Disney (DIS) and Roku out there by way of The Commerce Desk’s platform, strengthening the corporate’s attain with two of a few of the most vital streamers within the business.

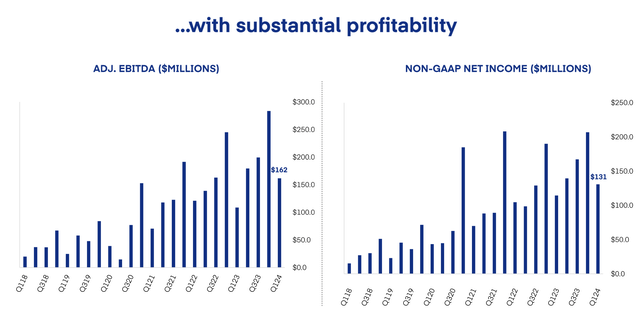

And as The Commerce Desk has grown, so has its profitability. In its most up-to-date quarter, The Commerce Desk’s adjusted EBITDA climbed 49% y/y to $161.7 million, with an adjusted EBITDA margin of 33% increasing 5 factors versus 28% within the year-ago quarter.

The Commerce Desk adjusted EBITDA (The Commerce Desk Q1 earnings deck)

And that is only the start of The Commerce Desk’s profitability leverage; already in Q2 the corporate has guided to adjusted EBITDA margins of 39%, bettering an extra six factors sequentially from Q1.

Dangers, valuation, and key takeaways

The core danger to the bull thesis for The Commerce Desk and its valuation are one and the identical: traders are already banking on large progress for this firm and assigning a wholesome premium to this inventory consequently.

At present share costs close to $96, The Commerce Desk trades at a market cap of $46.96 billion. After we internet off the $1.42 billion of money on the corporate’s newest stability sheet, The Commerce Desk’s ensuing enterprise worth is $45.54 billion.

In the meantime, for the present 12 months FY24, Wall Avenue analysts expect The Commerce Desk to generate $2.42 billion in income (+24% y/y), and subsequent 12 months in FY25 to develop an extra 20% y/y to $2.90 billion. This places the inventory’s valuation multiples at:

18.2x EV/FY24 income 15.7x EV/FY25 income

It is a steep valuation vis-a-vis different software program firms which can be rising at a ~20-30% y/y clip; however quite than seeing The Commerce Desk as in a bubble, I view the inventory because the beneficiary of multi-year tailwinds which can be pushing extra {dollars} into programmatic promoting spend. The corporate’s high-profile offers with media firms in Q1 is proof of its rising momentum, and its sharp adjusted EBITDA margin good points additional cement the case that this firm nonetheless hasn’t hit the part of maturity and slowdown but.

Keep lengthy right here and maintain using the uptrend.

{kind=link}