da-kuk

It has been 8 months because the final time I wrote about Fortinet, Inc. (NASDAQ:FTNT). Since then, the corporate has had a really unstable 2024. It was up +25% in March however dropped to -5% per week in the past. After the Q2 earnings launch, which we’ll focus on intimately, Fortinet’s shares have surged to extra cheap costs given the standard of the enterprise. In January, I rated the inventory as a purchase, and because of the current rise, now we have a 19.87% return in comparison with the S&P 500’s 10.69% and the 5.36% of the safety ETF I comply with essentially the most, the iShares Digital Safety UCITS ETF USD Acc.

Supply: Koyfin

Underlying Thesis

As I defined within the first article, The thesis for Fortinet is its nice popularity and experience in particular areas of cybersecurity, accompanied by a extremely scalable product portfolio, profitable penetration into new market niches like SASE, wonderful capital administration, and founders with over 20 years of expertise within the firm and the sector. We’re all conscious that cybersecurity is a really difficult sector for the generalist investor to know, which is why in this sort of firm, the administration groups play a essential position within the thesis. Thankfully for Fortinet, this could be its strongest level.

Within the article, we additionally speak in regards to the cycles that its {hardware} phase often experiences, which we’ll focus on later. Moreover, we cowl its ecosystem, which is the second key to the thesis. Within the phrases of my previous article:

In my view, the important thing energy of this firm lies in its unified platform, FortiOS, which integrates varied services and products somewhat than creating standalone options which are troublesome to combine. This not solely generates a community impact but additionally presents excessive switching prices for patrons, probably resulting in pricing energy. The ecosystem created by the corporate makes it indispensable for the client.”

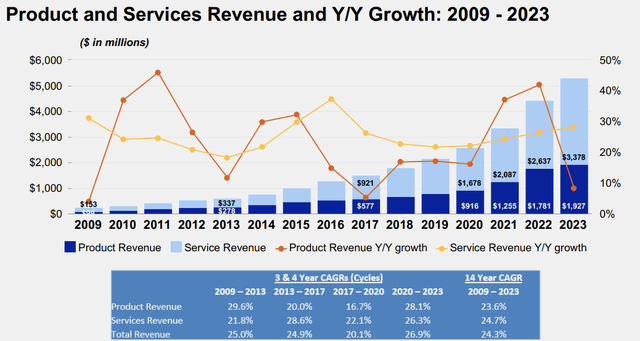

Supply: This fall’23 Investor Slides. Slide 21

Current Occasions

Let’s analyze the corporate’s Q2 outcomes. I may also use components of the transcript.

The general figures for the quarter have been fairly good, particularly standing out within the margins. The rise in margins has been because of a number of elements. They’ve managed to broaden margins on the backside of the cycle. It may be argued that as software program weighs extra within the gross sales combine, margins develop, however you even have some operational deleveraging as a result of drop in product gross sales. Due to this fact, I consider margins will proceed to broaden in future cycles. Additionally they had decrease OPEX bills (particularly in advertising bills), growing margins, however they are going to increase these once more as soon as demand picks up extra, which is one other approach of reinvesting within the enterprise.

Supply: Fortinet Investor’s Relations

Administration as soon as once more confirms one of many key factors of the thesis: the cross-selling and upselling of merchandise, making a a lot stickier ecosystem for its clients.

However on the opposite facet, we additionally see plenty of new alternative, whether or not within the OT space within the Unified SASE and in addition upsell, cross-sell that are all serving to driving, I might say, in all probability like a 90% buyer initially moved by a FortiGate getting the firewall and community safety market first, which now we have an enormous benefit over opponents.

However after that one, they’re maintaining increasing past the community safety, go to the opposite space. So that is what’s taking place for the Unified SASE for the Safe Op. And now the product, particularly on the FortiGate firewall facet we’re beginning to see form of return to regular or beginning rising with the market now.” – Ken Xie, Fortinet’s CEO and founder.

Supply: Writer’s illustration

My view of Fortinet’s product phase is sort of a Mr. Potato Head with software program items added on high, an instance of upselling. It additionally jogs my memory fairly a little bit of Nintendo with its Change console; the years with the very best {hardware} gross sales are accompanied by many software program gross sales. In a approach, that is additionally confirmed by the CEO.

So as soon as the product begins rising, as a result of product has a decrease gross margin, that in all probability will impression the margin, however the product can also be the main indicator of future service. In order that’s the place we form of additionally have been pleased to see the product additionally beginning rising now, which I feel going ahead with the product has a better proportion, that in all probability additionally will impression the margin.” – Ken Xie, Fortinet’s CEO and founder.

Supply: Writer’s illustration

Whereas all of that is constructive, I do not assume these are the principle explanation why the market drove Fortinet’s shares up 25% in a single session. One of many important causes is that they count on billings to return to a constructive progress development within the subsequent quarter. Billings are a number one indicator of gross sales, and it’s beginning to be discounted that now we have reached the underside of the cycle in {hardware}. 90% of those billings come from present clients, with over 80% being massive enterprises, that are typically extra resilient to financial cycles and have a tendency to chop again on important companies like cybersecurity.

And talking of the underside of the cycle: Gross sales for the quarter grew by 11%, however have been pushed by companies by 20%, therefore the file margins. Product gross sales decreased by 4%. The gross margin rises to 81%, with a product gross margin of 66%, primarily because of an elevated software program combine and decrease oblique prices. They’re additionally benefiting from generative AI, particularly of their menace evaluation and detection parts. Evidently the refresh cycle for the {hardware} phase is being pushed again to 2025 as an alternative of 2024, but the market has largely ignored this, doubtless as a result of enhance in billings.

The corporate additionally offered its steering for the total yr:

And once more, for the total yr, inclusive of the numbers we gave a second in the past, we count on billings within the vary of $6.400 billion to $6.600 billion; income within the vary of $5.800 billion to $5.900 billion, which on the midpoint represents progress of 10%. Service income remained of $3.975 billion to $4.025 billion, which on the midpoint represents progress of 18%.

Non-GAAP gross margin of 79% to 80%, Non-GAAP working margin of 30% to 31.5%. Non-GAAP earnings per share of $2.13 to $2.19, which assumes a share rely of between 767 million and 777 million. Capital expenditures of $320 million to $360 million. Non-GAAP tax price of 17% and money taxes of between $525 million and $575 million.” – Keith Jensen, Fortinet’s CFO.

They’ve additionally made two acquisitions throughout the quarter. They appeared fairly optimistic about them and have clearly discovered worth in these acquisitions, as they haven’t repurchased any shares regardless of current value declines. This is not one thing that worries me an excessive amount of, as they nonetheless have $1 billion approved for share buybacks, and Fortinet could be very opportunistic in executing these, as proven within the chart. The acquisitions will impression margins within the brief time period.

Supply: Koyfin

Having a robust administration crew centered on the long run lets you spend money on upcoming macrotrends no matter market opinions. Moreover, this creates alternatives for long-term traders who’ve carried out prior evaluation and know what they’ve of their portfolio. On this case, the next is true:

That is additionally you may see the Gartner analysis we identified, the convergence of community within the community safety additionally beginning or accelerating. So initially, I feel final yr, they are saying by 2030, the safe networking will likely be bigger than conventional networking. Now they are saying, 2026, 4 years forward, the safe networking will likely be bigger than the normal networking. In order that’s the place we actually make investments long run on this development. And with all this FortiOS, FortiASIC and making one of the best each equipment and infrastructure, the ASIC know-how and on the similar time, additionally attempt to make investments extra within the gross sales and advertising space to essentially catch the development and in addition hold gaining market share. So that is the technique to be forward.” – Ken Xie, Fortinet’s CEO and founder.

Fortinet continues to take a position and acquire market share in areas the place they’re already one of the best.

Safe networking clients are more and more acknowledged our FortiOS and FortiASIC know-how providing 5 to 10x higher efficiency than our opponents whereas enhancing safety effectiveness and offering a low complete price of possession.” – Ken Xie, Fortinet’s CEO and founder.

Their internally manufactured ASICs, particularly designed for his or her merchandise, present price financial savings and elevated energy, that are handed on to their clients in a type of shared economies of scale. In actual fact, they have not raised costs since early 2023 and have been securing higher offers for his or her clients thanks to those price financial savings. Moreover, the rise in gross sales of their firewalls lately serves as a Malicious program for subsequent upselling and ecosystem creation.

Supply: Q2’24 Investor Slides. (Slide 9)

Valuation

On this part, I will likely be transient as a result of I’ll proceed utilizing the annual information from 2023. I might try and create a Free Money Circulation estimate for 2024 and replace it to an element (4/12, the remaining months of the yr), but it surely would not add a lot worth, and I desire to be extra conservative utilizing present information. In any case, if we use a reverse DCF with a Terminal Progress Price of three% and a reduction price of 10% (the minimal I require for my investments), at present costs, it could counsel that the market is discounting a FCF progress of 13.5% for the subsequent 10 years. I consider this progress is sort of achievable, maybe not for this yr, however as soon as the cycle recovers, margins broaden, and so they proceed with good capital allocation, I feel this progress will likely be within the middle-lower vary of the vary I contemplate.

Nonetheless, after such a steep enhance, I doubt it’s going to rise rather more within the brief time period, and there could be a chance to purchase on a pullback, gaining some margin of security. For all these causes, I price the inventory as a maintain.

Supply: Writer’s Illustration

Dangers

These corporations will not be with out dangers, simply ask CrowdStrike, however I consider it is a widespread danger throughout all corporations within the sector and is determined by inner execution. The administration crew and company tradition at Fortinet reassure me on this regard.

I consider the best short-term danger to the corporate’s inventory value (as I do not assume it poses a excessive long-term danger) could be a deterioration within the {hardware} cycle or additional delays. They’ve said that they count on to start out recovering in 2025; if this does not occur, the inventory will endure. Nonetheless, this isn’t a long-term danger and will truly create funding alternatives if the inventory corrects consequently.

The opposite dangers are the identical as within the earlier article: distributor focus, manufacturing in Taiwan, the chance of {hardware} obsolescence in inventories, and competitors, because the cybersecurity sector is especially difficult. These are additional developed within the article.

Different Vital Graph

Fortinet’s efficiency over the past 10 years has been fully distinctive. A complete return of +1326% for its shareholders, which equates to a 30% CAGR. Drawdowns of 35% have been considerably widespread for the corporate, but it surely hardly ever exceeds that proportion of declines. The Value/FCF a number of proven by Koyfin does not appear essentially the most acceptable for Fortinet, as two changes have to be made. With the annual information from 2023, Fortinet had $1.4 billion in web money and can also be in an expansive CAPEX cycle, so this determine must be normalized. The adjusted a number of could be 28X, which, whereas excessive, I do not assume is overvalued.

Supply: Koyfin

Conclusion

Total, I consider Fortinet’s quarter has been excellent. They proceed to take a position long-term in efficient niches. Administration remains to be executing effectively, and capital allocation stays robust. The underside of the cycle is simply across the nook, and the next {hardware} refresh will drive a rise in software program gross sales and fortify the ecosystem in lots of corporations, finally resulting in increased recurring margins and returns for the corporate. I am happy to be a shareholder on this nice firm.

{kind=link}