Matteo Colombo

Funding replace

Following my final publication on STERIS plc (NYSE:STE) the inventory is +2.5% within the inexperienced after backing and filling into congestion. The corporate’s Q1 FY’25 numbers gleaned a number of insights that present a complete view into what to anticipate for the rest of the monetary yr. That report, titled “Stays on observe for sturdy fiscal 24″, outlined a number of bullish components within the debate, together with:

STE staged an upside transfer off lows in early ’23, the place I advocated shopping for the corporate at $214. Engaging fundamentals which are methodically rotated into extra market worth. Extremely FCF productive with a number of avenues to deploy money, albeit with out the high-return prospects of a much less mature firm.

It is a identify I’ve coated since 2020 right here on SA, try the coverages: (2020 right here, 2022 right here, right here and right here, 2023 right here and right here).

I stay a purchase on STE as a result of 1) modelling updates from its Q1 numbers [FY’24-’26E assumptions get to ~$1Bn in FCF each rolling 12mo with ~2% compounding growth in intrinsic business worth], 2) extremely productive of money circulation + makes use of capital properly, and three) valuations supportive to ~$270/share below these assumptions. Internet-net, reiterate purchase.

Determine 1. STE value evolution, 2023-date

TradingView

Q1 FY’25 earnings insights

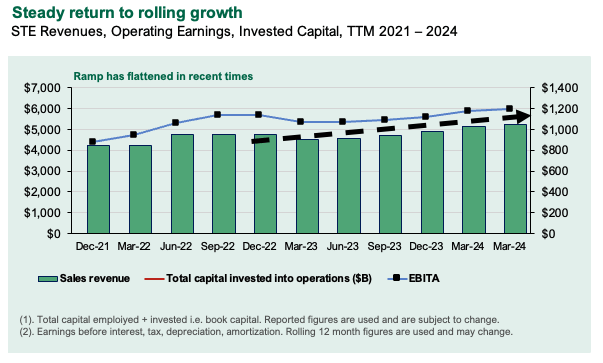

STE put up $1.3Bn in gross sales (+8%) underscored by a 270bps value enhance + FX tailwinds. Administration reiterated its FY25 outlook and calls for six.5-7.5% top-line progress (vs. consensus 1%) and eyes earnings of $9.05-$9.25 per share on this. The gross sales ramp is now constructive since FY’22 (Determine 2) and working earnings are following swimsuit.

Determine 2.

Firm filings

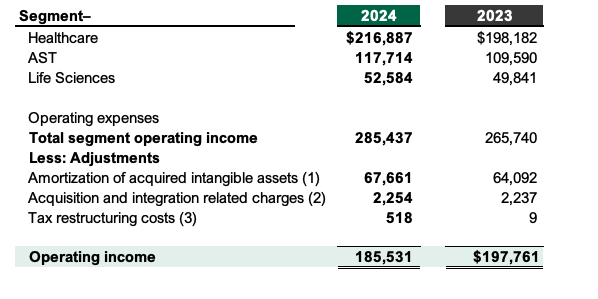

As to the phase takeouts, my notes embrace the next (see: Determine 3):

Healthcare revenues have been +10% to $901mm – this was pushed by 23% progress in serve + capital gear revenues. Administration mentioned volumes have been sturdy and that instrument belongings bought from Becton, Dickinson are beginning to pull weight. The Utilized Sterilization Applied sciences (“AST”) phase did $250mm of enterprise within the quarter (+7% YoY) with 24% upside in capital gear gross sales. This pulled to ~6.2% working earnings progress. Life sciences did ~2% income progress to $128mm – as a reminder, administration is cutting down this enterprise and so it isn’t shocking to see double-digit declines in cap. gear gross sales.

It pulled these gross sales to ~45.1% gross, which is 30bps decompression YoY as a result of higher value combine and value will increase. Working margins compressed ~20bps YoY off a excessive base in FY’23, however the combo of 1) larger insurance coverage prices and a pair of) compensation prices eroded margins – regardless of +$20mm EBIT YoY.

Determine 3.

Firm filings

Extra takeouts:

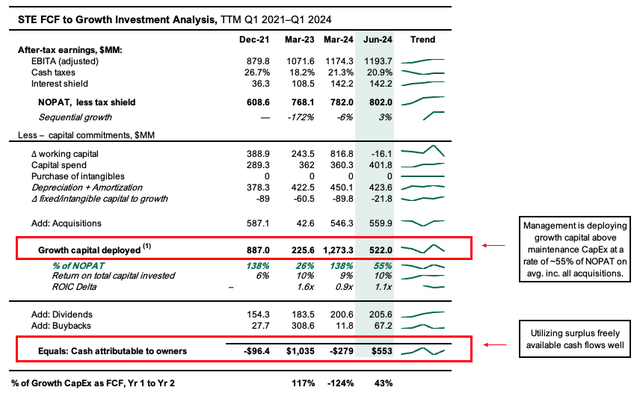

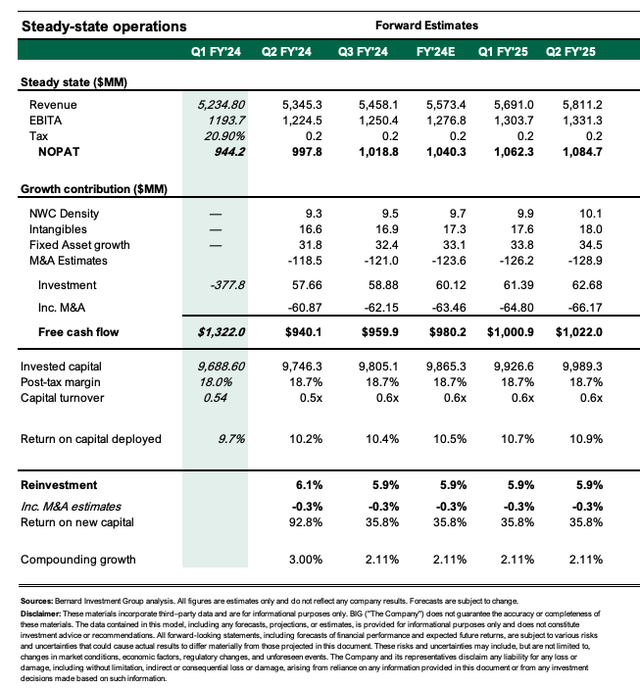

It recycled ~$108mm CapEx for ongoing investments in capability enlargement and operational effectivity. Following the divestiture of its Dental enterprise, debt excellent is ~$2.3Bn or ~1.6x EBITDA. It is a enterprise throwing off ~$1Bn in freely out there money circulation in spite of everything reinvestment necessities are thought of to take care of competitiveness and develop. This surplus funds 1) ongoing dividends + buybacks [which, in my view, are a good use of capital as I believe the shares are undervalued], 2) strategic acquisitions [the company made 13 bite-sized acquisitions during the quarter] and three) place the corporate to proceed investing in progress. My estimates are it has allotted $250mm-$1Bn each rolling 12mo since FY’21 particularly to investments above and past the upkeep degree of CapEx (approximated as the extent of depreciation + amortization – see: Determine 4). STE subsequently introduced its nineteenth consecutive yr of dividend will increase, elevating its quarterly dividend $0.57/share.

Determine 4.

Firm filings

My views of the corporate’s earnings are that they have been according to expectations and that it was an upside shock to see progress within the AST phase. Critically, this isn’t a high-growth or compounding enterprise. Quite, now we have secure and predictable money flows which are valued at a secure multiply by the market. There may be inherent worth on this on a predictability and visibility foundation. As such, the 2 key segments to regulate in my view are the AST and healthcare companies. Each are rising round 10% annualised and should current the enterprise with the chance to thoughts the acquisition pipeline in my view. Healthcare industries, significantly these concerned in capital gear markets, turning into increasingly fragmented, resulting in consolidation and buyouts. STE is well-positioned to capitalise on such selective alternatives, in my view, and the truth that it’s such a extremely cash-productive identify signifies to me that it’s trigger-ready and may opportunistically act when wanted. It doesn’t preserve a excessive degree of money stability on the stability sheet (it doesn’t have to as a result of money is available in rapidly, and better quantities – money available was solely 10% and a pair of% of present belongings and whole belongings final quarter respectively). In that vein, the enterprise is properly positioned to proceed its persistent degree of progress in my opinion.

Pretty valued with secure multiples

The enterprise is routinely valued at ~2.6x EV/IC and at the moment trades at ~27x NOPAT, down on the final 2yrs common. My view of the enterprise is value $270 per share at this time on the mix of 1) its monetary progress, 2) the conversion of earnings to FCF which are 3) recycled into the enterprise and/or again to shareholders. The principle issue, if the enterprise is very FCF productive, warranting a long-term view with respect to valuing it.

Valuation insights

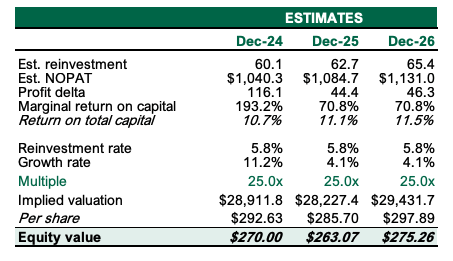

My views are that administration will make investments round $60 million each rolling 12mo to compound the asset base. I envision edge to provide round 10% to 11% return on marginal capital, reinvesting 6% of post-tax earnings at these charges. This warrants a circa 4% compounding worth of the intrinsic value of the enterprise. I do imagine there may be worth in compressing the present multiples to 25x, which nonetheless will get us up $270/share on my FY’24-’26E estimates.

As well as, my estimates have the corporate throwing off round $1 billion in free money circulation each rolling 12 months. Discounting the worth of this to the current at a 12% hurdle price out over the approaching 5 years, arrives at an identical analysis of round $270 per share. Given there may be confluence round this determine, I revise my value goal on the enterprise as much as $270 per share, up from $250 earlier. The revised by score is supported by the truth that expectations are moderately impartial (EV/EBIT of 27x is under 5yr avg. of 32x, and value momentum is flat), however that the standard of the enterprise is excessive.

As such, the valuation is most delicate to the funds STE administration can redeploy again into operations. Any extra alternatives for administration to reinvest – and extra so if it does – must be given excessive marks.

Determine 5.

Creator estimates

Dangers to funding thesis

Key dangers to the funding thesis embrace 1) gross sales progress lower than 2% as this limits the flexibility of administration to re-deploy funds into the asset base and develop earnings, 2) buyers paying lower than 22x NOPAT which brings the valuation under present market worth on my ahead estimates, and three) the broader set of macroeconomic issues that have to be made with all fairness evaluations proper now, specifically the inflation/charges axis, unemployment knowledge, and geopolitical dangers that might spill over into broad fairness markets.

Buyers should realise these dangers in full earlier than continuing any additional.

In brief

STE stays a purchase in my opinion after it is Q1 FY ’25 numbers, which exhibit a sample of constant free money circulation manufacturing and secure earnings and capital employed within the enterprise. It is a firm throwing greater than $1Bn out there money each rolling 12-month interval in spite of everything reinvestment and progress funding issues are factored in. It’s arduous to compete towards an funding proposition with these financial traits as they supply enterprise optionality to mine the acquisition pipeline, make investments for efficiencies, or return capital to shareholders by way of dividends and/or buybacks (which it has been diligently doing for a few years now). My view if the enterprise is value round $270 per yr at this time, round 15% upside potential on the time of writing. Internet-net, reiterate purchase.

Appendix 1. Ahead assumptions, CY 24 – ’26E.

Creator

{kind=link}