mgkaya

Will the Federal Reserve decrease its coverage charge of curiosity or not?

That’s the query.

However, as I maintain writing, is that actually the query that we ought to be asking?

Some analysts are taking an extended have a look at the actions within the M2 cash inventory.

Considerations right here is that the M2 cash inventory has been declining for a considerable time frame.

Let’s take a look at the chart.

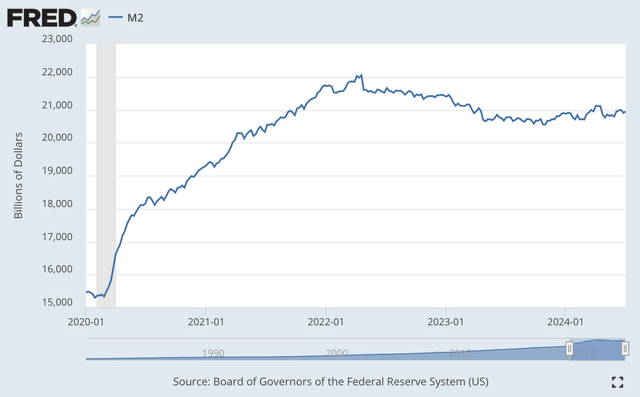

M2 Cash Inventory (Federal Reserve)

The height of the M2 cash inventory numbers comes within the week of April 18, 2022…just some weeks after the Fed begins its present efforts of quantitative tightening.

The M2 cash inventory reached $22,048.8 billion in that week.

within the week of July 1, 2024, the M2 cash inventory totaled $20,947.5 billion, down $1,101.3 billion from the height.

This 5.0 % downward motion within the M2 cash inventory came visiting 27 months.

Traditionally, this size of a downturn in cash inventory development was related to an financial recession.

The issue with this conclusion is that over the previous 4 years, ending within the first week of July 2024, the annual compound charge of development of the M2 cash inventory was greater than 8.0 %.

This charge of development of the M2 cash inventory might be related to a interval of considerable inflation. And, the U.S. financial system has skilled a interval of inflation throughout this time interval.

However, the query may then be requested, why wasn’t inflation over this time interval worse than was skilled?

The reply is that individuals didn’t spend cash throughout this era as quickly as they’d achieved earlier than.

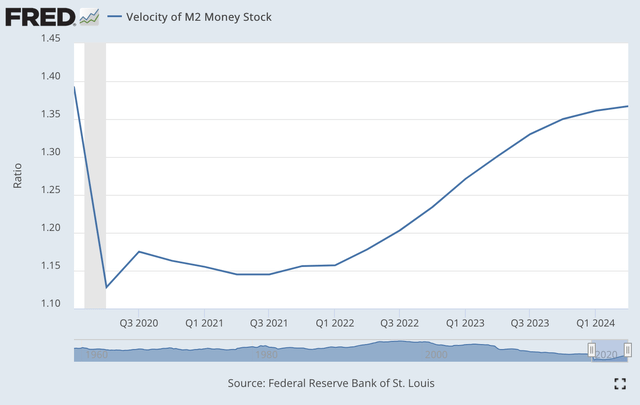

Let’s now check out the speed of circulation for the M2 cash inventory.

Velocity of M2 Cash Inventory (Federal Reserve)

As could be seen, whereas the M2 Cash Inventory was rising very, very quickly, the turnover of the cash inventory dropped precipitously in the course of the quick recession coming in 2020 and solely moved again modestly till the Fed started its effort at quantitative tightening.

As soon as the quantitative tightening started, the M2 velocity of circulation started rising.

Nonetheless, the M2 velocity has not reached the extent it was at simply earlier than the newest recession.

In impact, the M2 cash inventory has grown very, very quickly over the previous 4 years, however…the M2 cash inventory has probably not been “turned over” the best way it has prior to now.

The M2 cash inventory has grown considerably like a “bubble” however the financial system has probably not felt the complete “thrust” of this rise within the M2 cash inventory as much as this cut-off date.

Sure, the Federal Reserve has achieved some work to take away all of the reserve cash it despatched into the financial system, but when folks actually have been spending cash on the charge that they’d prior to now…if the speed of circulation had remained at ranges reached earlier than the final recession…inflation would have been a lot, a lot worse.

And, if the speed of circulation continues to rise and regain the extent it was at earlier than the final recession…effectively…inflation may start to speed up once more.

It is a cause why the Federal Reserve wants to keep up the next degree of its coverage charge of curiosity.

If the speed of circulation continues to rise, look out inflation!!!

Quantitative Tightening

So, what’s the Federal Reserve doing about its quantitative tightening stance?

Earlier the Fed indicated that it would start decreasing the quantity that it was decreasing the securities portfolio by every month.

The beginning date appeared to be round June 2024.

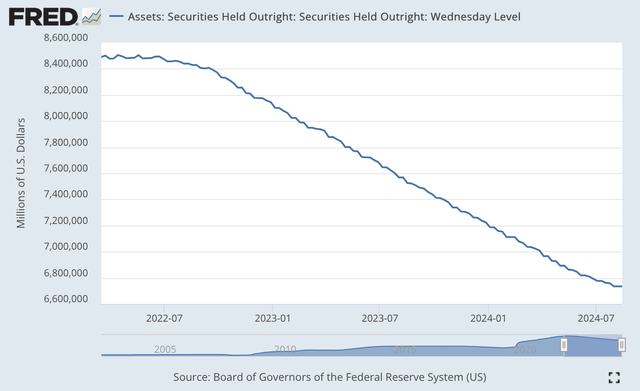

From June 6, 2024, to August 14, 2024, the Fed’s securities portfolio has solely declined by $84.0 billion.

Securities Held Outright (Federal Reserve)

One can’t actually see the shift clearly from this chart, however, the curve appears to be flattening out on the far right-hand nook.

It appears just like the Fed is doing a bit little bit of “slowing down” within the discount effort.

If the Fed has actually slowed down this discount marketing campaign, part I of the quantitative tightening was carried by from the center of March 2022 till the top of Could 2024… twenty-six months.

It is a very prolonged interval of financial “tightening.”

And, now part II of the quantitative tightening started in June 2024, so we’re within the third month of this part.

Nonetheless, the massive query that continues to be is…how rather more “tightening” does the Federal Reserve need to do?

The Federal created the massive “bubble” in reserves famous above. That’s what received the M2 cash inventory rising.

If the speed of circulation of the M2 cash inventory continues to choose up…inflation charges may take off once more.

That is the very last thing the Federal Reserve would need, particularly in spite of everything the hassle it has put into the quantitative tightening of the previous two years, plus.

If one appears on the inflation image from this angle, the Fed appears prefer it nonetheless has a bit of labor left to do.

Possibly reducing the coverage charge of curiosity may kick off an angle change within the financial system, one which kicks off an increase within the velocity of circulation…an increase that will certainly end in a rise within the inflation charge.

It simply appears to me that the Federal Reserve isn’t wherever near “declaring victory” and transferring on to higher financial ease and decrease rates of interest.

The reality is…the Federal Reserve pumped tons and plenty of cash into the monetary system to fight the issues related to the Covid-19 pandemic and the next recession.

The Fed has achieved effectively to this point…however, there stay tons and plenty of “extra funds” hanging round within the financial system that would set off the inflation button as soon as once more.

Buyers?

Properly, traders have been ready for the Fed to start out reducing its coverage charge of curiosity.

The look ahead to a transfer has prolonged effectively past the time that traders believed that adjustments would begin to be made.

But inventory costs continued to rise.

Why did inventory costs proceed to rise?

Due to all the cash that also exists inside the monetary system.

Buyers have continued to guess on shares, despite the fact that the Federal Reserve has gone by greater than two years of quantitative tightening.

My feeling is that except one thing else occurs to generate a response, a method or one other by the Fed

is that the Fed will “carry on, keepin’ on” to proceed the discount of its securities portfolio, with possibly an rate of interest discount right here or there.

If the Fed continues on this approach, I see no cause for traders to cease placing cash within the inventory market…and inventory costs will proceed to hit new historic highs.

{kind=link}