Miguel Perfectti/iStock Editorial by way of Getty Pictures

Editor’s notice: In search of Alpha is proud to welcome Oriol Argelich as a brand new contributing analyst. You may change into one too! Share your greatest funding thought by submitting your article for assessment to our editors. Get printed, earn cash, and unlock unique SA Premium entry. Click on right here to seek out out extra »

With renewed market volatility and considerations over an impending U.S. recession, dividend-oriented traders can look abroad to Spain for an excellent income-producing play. Repsol (OTCQX:REPYY) (OTCQX:REPYF) is a Spanish, built-in oil and gasoline agency based in 1987. Using 25,000 employees, it is one of many largest corporations in Spain and ranked because the 332nd largest public firm on this planet – but nonetheless little recognized by mainstream traders. With a ~7% dividend yield and new initiatives put in in each the U.S. and Mexico to drive future development, in addition to a variety of renewable power investments, I’m giving Repsol a Purchase score: this can be a nice inventory so as to add to your portfolio, particularly as the corporate has already dedicated to elevating its dividend subsequent yr.

Firm Overview

Repsol operates by way of the next enterprise segments:

Exploration and Manufacturing (Upstream or “E&P”): Actions for the exploration and manufacturing of crude oil and pure gasoline reserves, in addition to the event of low-carbon geological options (geothermal, carbon seize, storage, and use, and so on.).

Industrial: Actions involving oil refining, petrochemicals, and the buying and selling, transport, and sale of crude oil, pure gasoline, and fuels, together with the event of recent development platforms equivalent to hydrogen, biomethane, sustainable biofuels, and artificial fuels.

Buyer: Companies involving mobility (gasoline stations) and the sale of gasoline (gasoline, diesel, aviation kerosene, liquefied petroleum gasoline, biofuels, and so on.), electrical energy and gasoline, and lubricants and different specialties.

Low-Carbon Era (LCG): Low-emissions electrical energy era and renewable sources.

Manufacturing and New Progress Initiatives

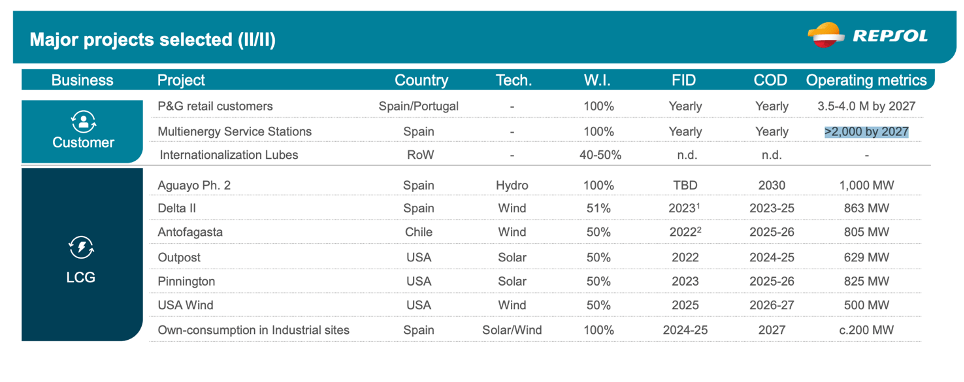

The corporate is planning to create extra worth by way of its manufacturing by beginning up new wells within the unconventional Marcellus asset (United States), the acquisition of the remaining 49% of Repsol Sources UK (RRUK), the acquisition of Tomoporo-La Ceiba (Venezuela), and the commissioning of recent wells in Colombia and Libya.

In the course of the first half of the yr, Repsol has additionally made vital strides in creating key hydrocarbon manufacturing initiatives, securing future competitiveness with an anticipated output of round 550 barrels of oil equal per day (kboe/d) by way of 2027. Notable achievements embody initiating the preparation section for the Polok and Chinwol discoveries in Mexican waters and commencing engineering work on the Sakakemang gasoline venture in Indonesia.

Moreover, Repsol has finalized its funding determination for the Monument venture in U.S. waters of the Gulf of Mexico and has elevated its stakes within the Monument, Bobcat, and Lucille initiatives in the identical area. First oil for the Monument venture is anticipated in 2026.

Repsol Upstream coverage is to cut back mounted prices and create effectivity, prioritizing the initiatives that create worth over whole manufacturing. The money generated per barrel produced is deliberate to extend by 30% by 2027, supported by the entry into manufacturing of the Leon_Castille venture (2025) within the U.S. Gulf of Mexico waters, and the Pikka venture in Alaska in 2026.

In July, Repsol and its associate (the Italian Eni) introduced a significant discovery in Mexican waters, the Yopaat- 1 nicely, with preliminary estimates indicating 300-400 million barrels of oil equal (Mboe) in place, together with oil and related gasoline. However along with all of those ongoing investments into conventional oil and gasoline discoveries, the corporate additionally has various LCG and renewable power initiatives. It has began producing 100% renewable fuels on an industrial scale on the first plant (situated in Cartagena) with a capability of 248 kta. In 2025, a second plant in Puertollano will be part of the plant in Cartagena. After an funding of €120 million and industrial complicated can be transformed to supply 240,000 tons of renewable fuels (240 kta). Repsol additionally plans to copy this in a 3rd industrial heart in Spain earlier than 2030.

As of June 30, the corporate has reached 342 stations with 100% renewable diesel availability: 310 in Spain and 32 in Portugal. Repsol is on monitor to achieve the objective of 600 stations by the top of the yr and 1.500 by 2025. I feel these additions will make a significant contribution to Repsol’s portfolio, which counts a complete of 4927 stations (525 in Peru; 207 in Mexico and 4.195 within the Iberia area)

Additionally, I consider biomethane and renewable power may even be necessary for the decarbonization of Repsol’s industrial complexes, utilizing them as uncooked materials to supply renewable fuels. The most important producer and shopper of hydrogen on Iberia (Spain & Portugal), plans to achieve an equal manufacturing of 700 MW by 2027 and a máximum of two.400 MW by 2030. To realize this, it can set up electrolyzers at 5 industrial facilities in Spain. In 2023, Repsol launched its first electrolyzer at Petronor refinery (Vizcaya) with a capability of two.5 MW; and in July 2024 Repsol acquired €315 million for 2 extra, Bilbao (100 MW) and Cartagena (100MW).

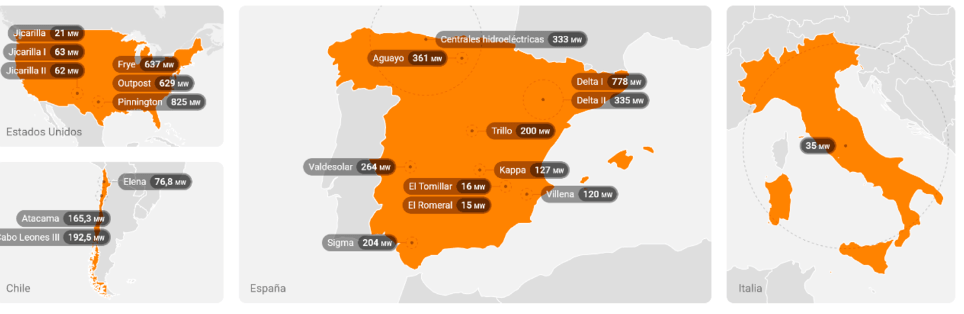

In the USA, Repsol has closed the acquisition of the renewable power venture developer ConnectGEN and accomplished the development of its largest photovoltaic photo voltaic plant to this point, Frye, with a capability of 637MW, which joins Sigma (204MW) in Spain.

Repsol has 60,000 MW of initiatives in growth, of which 2,870 MW are already below development. Its put in renewable capability has elevated by 54.6%, reaching 3,118 megawatts (MW). In the course of the semester, the corporate elevated the amount of electrical energy offered by 47%, reaching 3,130 GWh. By the year-end, Repsol expects to attain 4 gigawatts of whole put in capability by and between 9-10 GW by 2027 (50% within the Iberian Peninsula and 30% within the U.S.). As a part of Repsol’s technique to lock in returns, they already agreed a long-term Buy Energy Settlement (PPA) for 89% of the output from the Fyre venture. They’ve 2 different main photo voltaic initiatives below development in Texas, Outpost (629 MW) with anticipated business date between 2024 and 2025, and the Pinnington facility (825 MW) with deliberate start-up between 2025 and 2026.

Repsol renewable belongings (Repsol web site)

Repsol has 2.4 million electrical energy and gasoline clients in Spain and Portugal (9% greater than on the finish of 2023). Under, you may see Repsol’s essential initiatives and the capability the corporate will be capable of add.

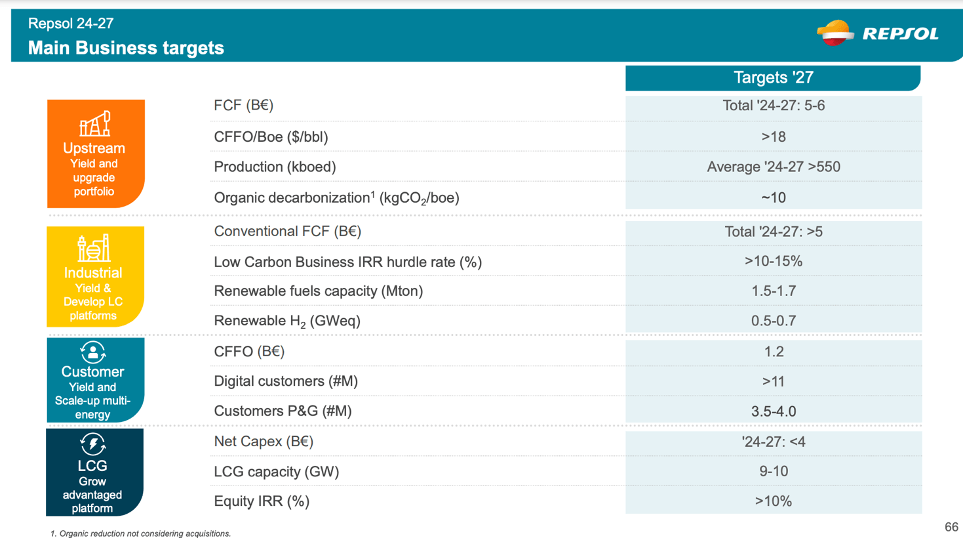

Repsol strategic plan 2024-2027 (Repsol presentation) Repsol strategic plan 2024-2027 (Repsol strategic plan) Repsol essential enterprise targets (Repsol strategic plan)

In my opinion, all of those initiatives present concrete help for the truth that Repsol continues to push development initiatives ahead, regardless of a macro image that has just lately been difficult for its sector.

Newest monetary traits and dividend improve

Like a lot of the remainder of the oil & gasoline sector, Repsol has been below stress from declining Brent oil costs. It is value noting, nevertheless, that the corporate has elevated its dividend amid solely very slight declines in EBITDA.

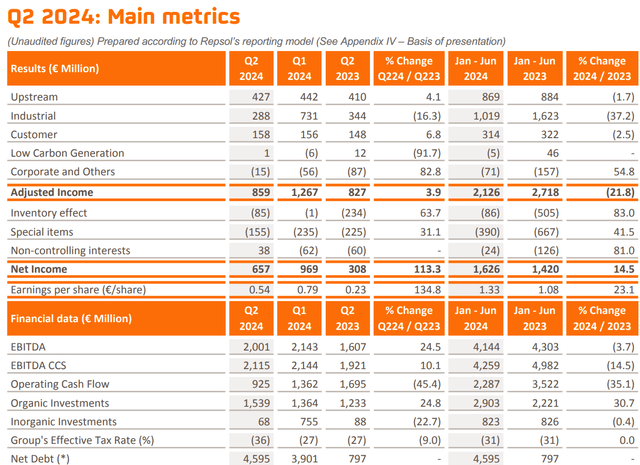

Repsol achieved a web earnings of €1,626 billion within the first half of the yr, representing a rise of 14.5%. The EPS for the primary half amounted to €1.33 per share, growing by 23.1%.

However when adjusting for the FX impacts on international tax belongings and oil costs on held stock, adjusted earnings – which the corporate makes use of as the most effective measure of working efficiency – was €2,126 billion, -21.8% decrease than the primary six months of 2023, pushed by decrease gasoline costs and decrease refining margins that primarily affected the commercial sector, whose outcomes fell by -37% in comparison with 1H’23.

Repsol Q2 outcomes (Repsol web site)

Regardless of the difficult setting in a number of segments of its enterprise, the group continues with its coverage of rewarding shareholders, which is a sign of its confidence in robust earnings forward. In my view, the corporate can obtain a return to top-line and earnings development in various methods. Normalization in oil costs might present super earnings aid, particularly if Center East tensions proceed and restrict provide (Brent crude is at multi-year lows not seen since 2021, and has been falling since summer season 2022). As well as, rising renewable power demand and maturing manufacturing of the current initiatives and wells mentioned within the earlier part might additionally assist to drive income development.

On August seventh, Repsol started a second buyback program for 20 million shares, along with the 40 million already repurchased because the starting of the yr. Since 2022, Repsol has redeemed 350 million shares, representing 22.9% of shares excellent.

On high of buybacks, the corporate additionally paid €0.90 in dividends per share in two payouts: €0.40 per share in January and €0.50 per share in July. That is 30% greater than the identical interval in 2023.

For 2025, the oil firm has dedicated €1,128 billion as a money dividend and plans to distribute €0.975 gross per share, which represents a rise of 8% in comparison with 2024 and represents a ahead yield of ~8% towards the present share value. In whole, the group plans to allocate €4.6 billion to money dividends till 2027. That is complemented by share buybacks and redemptions valued at as much as €5.4 billion, aiming to attain a shareholder distribution vary of 25% to 35% of the interval’s working money stream.

Regardless of the excessive yields, I am comforted by the truth that the corporate has greater than ample working money stream to help it. Within the first half of 2024, the corporate generated €2.29 billion in working money stream and paid out solely €533 million for dividends (plus €598 million for buybacks), indicating fairly ample dividend protection to help its general capital returns program.

Working money stream throughout 2Q24 was €925 million, €770 million decrease than in the identical interval of 2023, primarily because of the money outflow associated to the acquisition of the remaining 49% stake in Repsol Sources UK and the settlement of the arbitration battle with Sinopec. Excluding this impact, money stream elevated by €216 million in comparison with 2Q23.

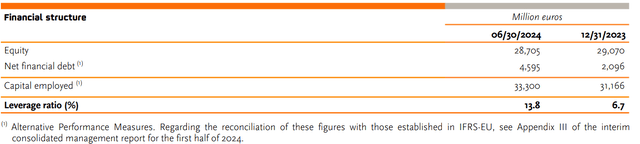

Repsol is strongly dedicated to renewable energies. Investments elevated by 30% in comparison with the primary half of 2023, with web debt standing at €4,595 billion.

The leverage ratio elevated to 13.8% in comparison with 6.7% in December 2023, and liquidity stood at €9,669 billion (together with undrawn credit score strains), representing 3.09 instances the short-term debt maturities, in comparison with 2.85 on the finish of 1Q.

Leverage ratio (Repsol’s web site)

Repsol Valuation

The current market decline has left Repsol’s share value at $14.04 making it a really enticing purchase, contemplating each its dividend and general earnings energy. It is an excellent worth funding that’s buying and selling decrease than the broader inventory market, its personal historic valuations, in addition to different power friends.

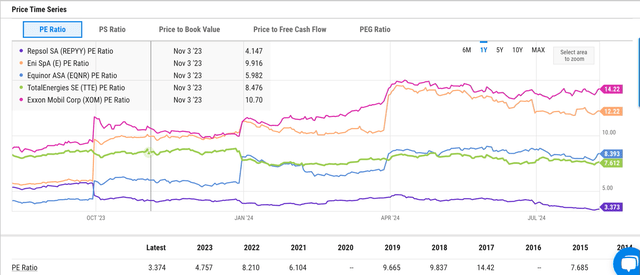

REPYY’s value is 17.10% beneath its historic valuation. The present inventory value is decrease relative to REPYY’s earnings and gross sales than it has traditionally traded. The P/E ratio is 3.374, a lot decrease than its 5-year common of 8.55. Different corporations within the sector, equivalent to ENI S.p.A., Exxon Mobil Corp, or Shell PLC, are within the 12-14 vary.

PE trade ratios (YCharts)

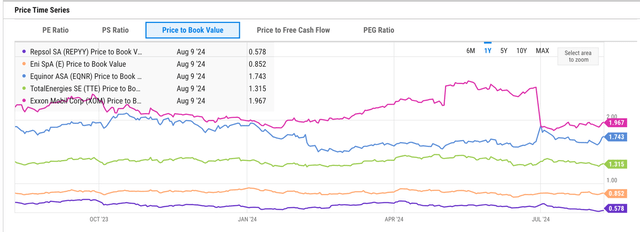

With a market cap of $16.17 billion, the Worth to Guide worth is 0.57, decrease than its common of 0.67 during the last 5 years and clearly decrease than different corporations within the trade.

Business Worth to Guide Worth (YCharts)

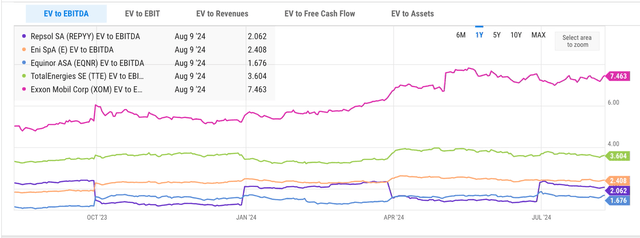

The EV to EBITDA is 2.062 as of August ninth, beneath the 5-year common of three.2.

Business EV/EBITDA (YCharts)

Within the context of stabilizing Brent costs and normalizing refining margins, I consider Repsol is well-positioned to take care of its shareholder remuneration coverage and return the share value to no less than the mid-range of $17. Furthermore, Repsol is betting closely on renewable power, which presents potential development alternatives sooner or later.

From my viewpoint, the inventory is buying and selling at a heavy low cost. TTM EPS is €2.70 per share. If we assume 8% development on earnings in 2025, (notice that the corporate doesn’t present a ahead outlook due to the volatility of power costs, however that is in-line with the corporate’s deliberate dividend improve), subsequent yr’s EPS can be €2.92.

If we apply a PE a number of of seven, extra in keeping with Repsol’s 5-year common and with the multiples of TotalEnergies SE (TTE), Eni S.p.A. (E), or Exxon Mobil Corp (XOM), we get a value goal of €18.9, or ~$21 in USD phrases for the ADR.

A dividend low cost model-based valuation yields the same reply. Following Repsol’s Strategic plan 2024-2027, we are able to anticipate dividend per share (DPS) to extend 3% yearly. Assuming a price of capital of 8% (common inventory market return) and a 3% charge of development for earnings (secure payout ratio) we’ve €0.975 FY25 DPS / (8% – 3%) = €19.50 / share (~$21). $21 would symbolize ~50% potential upside towards the present share value, plus dividends.

Dangers and Key Takeaways

After all, Repsol’s YTD declines are a mirrored image of various dangers that the corporate faces. New initiatives and investments that Repsol has spent billions to ramp up might take longer to change into productive. As well as, power costs might stay low if macro traits proceed to be weak, dampening international demand. These might affect Repsol’s dedication to spice up its dividend additional in 2025 and past.

Nonetheless, the corporate deserves credit score for its plans to dramatically scale its 100% renewable vegetation in its dwelling market on the Iberian peninsula, whereas additionally investing in different renewable power websites within the Americas.

Contemplating the wealthy ~8% ahead yield on this inventory, the ample dividend protection on high of aggressive share buybacks that benefit from decrease share costs, and a less expensive valuation towards different power friends, I consider Repsol is a good purchase.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. trade. Please pay attention to the dangers related to these shares.

{kind=link}