kirstypargeter/iStock through Getty Pictures

Denali Therapeutics Inc. (NASDAQ:DNLI) is a clinical-stage biotech growing neurodegenerative illness therapies. The corporate’s principal worth driver is its mind supply platform, which makes use of a biomarker-driven drug growth method. DNLI’s proprietary Transport Car [TV] know-how overcomes the standard limitations of delivering drugs throughout the blood-brain barrier [BBB]. This manner, DNLI can present the mind with therapeutic molecules for situations like MPS II, Alzheimer’s, Parkinson’s, and different neurodegenerative diseases. It is a helpful IP that uniquely positions DNLI in neurodegenerative purposes. I imagine DNLI has sufficient sources to ultimately attain a possible FDA approval on not less than one in every of its drug candidates. Thus, I deem it DCA “purchase” for buyers who perceive the inherent biotech dangers.

Biotech Supply Platform: Enterprise Overview

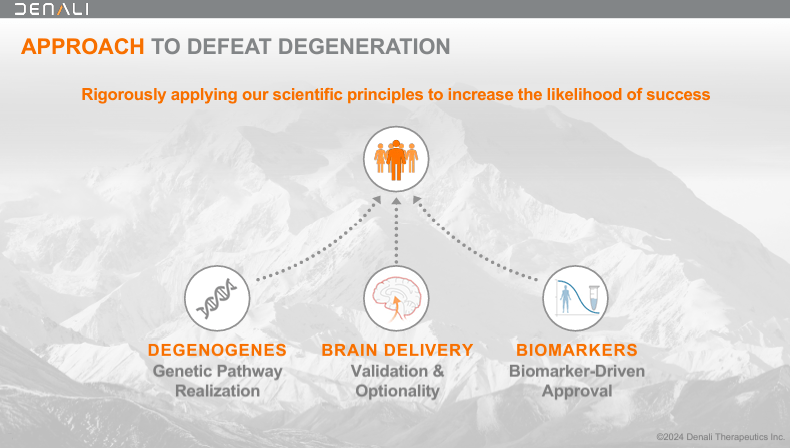

Denali Therapeutics Inc., based in 2015, is a biotechnology firm primarily based in South San Francisco, California. DNLI develops therapies for neurodegenerative situations utilizing a threefold technique: 1) mind supply, 2) leveraging genetic pathway potential, and three) biomarker-driven drug growth. DNLI concentrates on genetic pathways in power neurodegenerative situations to develop focused molecular therapies. The corporate accomplishes this by way of its proprietary TV platform.

Supply: Company Presentation. August 2024.

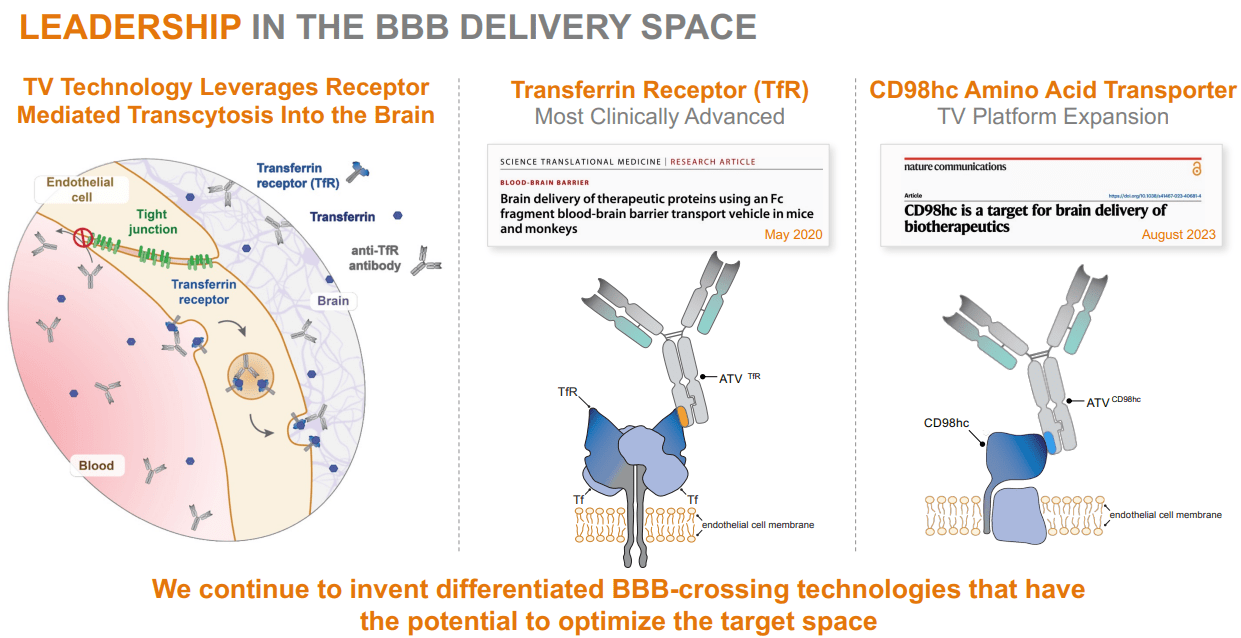

Subsequently, DNLI’s mind supply technique makes use of its TV platform by way of intravenous administration. This delivers massive therapeutic molecules, corresponding to antibodies, enzymes, and oligonucleotides, throughout the Blood-Mind Barrier [BBB]. The BBB is a protecting barrier that blocks most substances from coming into the mind. DNLI’s TV know-how facilitates the transport of varied therapeutic molecules, together with enzymes, antibodies, and oligonucleotides, throughout the BBB for therapeutic results on neurodegenerative illnesses. Its Fc area molecules then bind to particular transport receptors on the BBB and transfer from the bloodstream into the mind.

Supply: Company Presentation. August 2024.

The distinctive side of DNLI is that it may take its engineered molecules throughout the BBB, distributing them successfully into the mind. This manner, DNLI can goal key illness pathways, together with lysosomal capabilities, glial biology, and mobile homeostasis. Furthermore, DNLI makes use of biomarkers in its early analysis, affected person choice, and dosage selections. Biomarkers are key as a result of they assist categorize sufferers into phenotypes, guaranteeing optimum affected person populations for trials. This manner, DNLI maximizes its probabilities of assembly medical endpoints, which is important for acquiring regulatory approval.

Main Product Candidates

Considered one of DNLI’s main drug candidates is DNL343 for ALS. It’s price highlighting that the ALS market is projected to achieve $1.3 billion by 2029, largely as a result of earlier analysis and intervention. ALS is a progressive neurodegenerative situation affecting motor neurons, resulting in muscle weak point and paralysis. At present, there are six accredited therapies for ALS, the latest being Biogen’s (BIIB) Qalsody, which prices $14,230 per dose. Nonetheless, DNLI’s DNL343 is a promising small molecule that prompts eIF2B. This activation regulates mobile protein synthesis, which reduces mobile stress and slows down motor neuron dying in ALS.

In concept, DNLI may carve out a distinct segment in ALS. Its motion mechanism differs from Biogen’s Qalsody, which targets the SOD1 gene fairly than eIF2B. DNLI estimates that DNL343 for ALS may attain peak gross sales of $1 billion to $5 billion, however I’m considerably skeptical. First, the ALS market doesn’t seem as huge, neither is DNL343 the one accessible therapy. As an illustration, AbbVie’s (ABBV) ABBV-CLS-7262 additionally targets elF2B, and it’s a a lot better-capitalized competitor.

Supply: Company Presentation. August 2024.

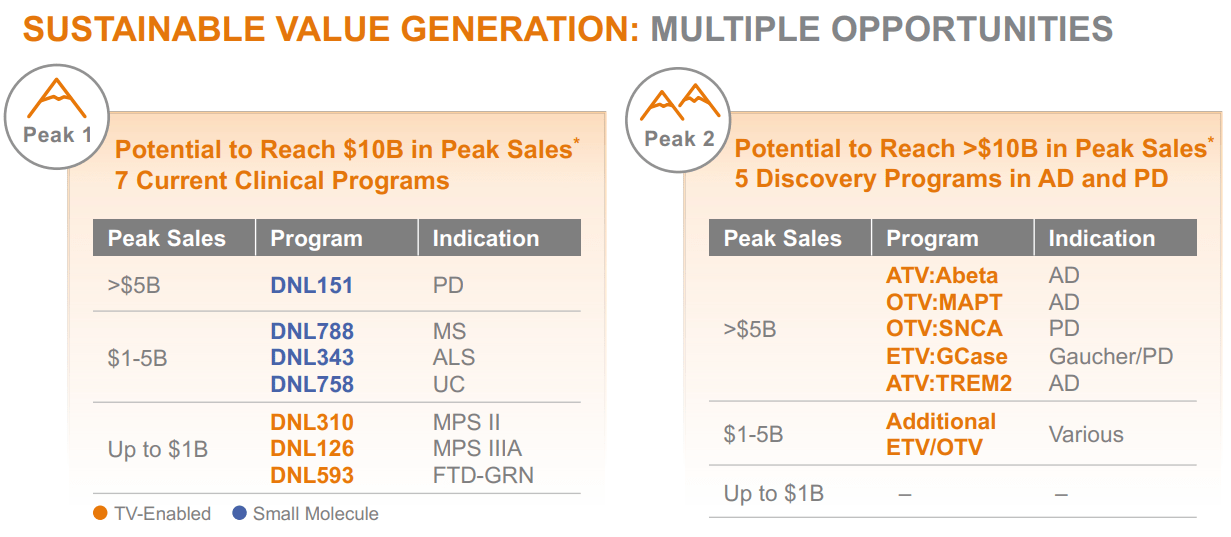

Nevertheless, in August 2024, DNLI’s company presentation highlighted that DNL343 isn’t its solely promising drug candidate. Its clinical-stage drug portfolio additionally has DNL151 for Parkinson’s Illness [PD], which is estimated to have potential peak gross sales of over $5 billion, contingent on being efficiently developed and commercialized. Likewise, DNL788 targets a number of sclerosis [MS], with forecasted peak gross sales at about $1 billion to $5 billion. Lastly, DNL310 for MPS II, DNL126 for MPS IIIA, and DNL593 for FTD-GRN may every generate as much as $1 billion in gross sales.

Worth Driver: Transport Applied sciences

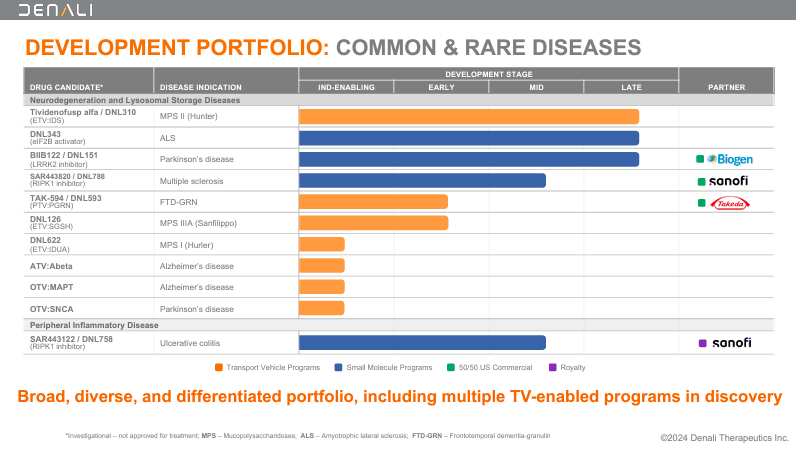

Nonetheless, the frequent theme amongst these drug candidates is that they leverage DNLI’s transport applied sciences. In actual fact, DNLI has secured partnerships utilizing its proprietary platform. As an illustration, SAR443820, or DNL788, is in mid-stage medical growth in collaboration with Sanofi. DNL788 acts as a Receptor-Interacting Protein Kinase 1 (RIPK1) inhibitor, which addresses inflammatory and neurodegenerative situations like MS. MS is a power autoimmune illness that causes neurological harm because the immune system assaults the myelin sheath of nerves. By inhibiting RIPK1, DNL788 reduces irritation and protects nerve cells, halting MS development.

Supply: Company Presentation. August 2024.

Equally, DNLI’s Peripheral Inflammatory Illness program contains SAR443122 or DNL758. DNL758 can be a RIPK1 inhibitor developed with Sanofi that targets the inflammatory processes in UC. UC is a power bowel illness that causes irritation and ulcers within the colon and rectum. Thus, DNL758 makes an attempt to cut back the harm attributable to UC. Likewise, DNL151 was developed with Biogen as a Leucine-Wealthy Repeat Kinase 2 (LRRK2) inhibitor. DNL151 is indicated for PD as a result of it inhibits the LRRK2 protein linked to dopamine neuron degeneration.

DNLI’s proprietary platform additionally works for uncommon genetic illnesses. As an illustration, DNL126 is an early-stage drug for Mucopolysaccharidosis IIIA (MPS IIIA), often known as Sanfilippo syndrome sort A. Right here, DNLI makes use of its Enzyme Transport Car [ETV] know-how to ship the poor enzyme N-sulfoglucosamine sulfohydrolase [SGSH] on to the mind. However, DNL593 targets Frontotemporal Dementia [FTD] by growing progranulin ranges, slowing illness development. DNL593 makes use of the corporate’s Protein Transport Car [PTV] know-how to ship therapeutic proteins throughout the BBB. Likewise, DNLI has different variations of its transport know-how, corresponding to DNL622, which targets beta-amyloid (Abeta) proteins accountable for plaque formation in AD sufferers. DNL622 targets beta-amyloid proteins linked to plaque formation in AD. DNL622 can be probably helpful as a result of it targets alpha-synuclein in AD and PD.

Pretty Valued: Valuation Evaluation

From a valuation perspective, DNLI trades at a $3.3 billion valuation, making it a mid-sized biotech in its sector. Its steadiness sheet exhibits $74.7 million in money and equivalents and $821.4 million in short-term investments. This totals $896.0 million in accessible short-term liquidity with no monetary debt and solely $115.5 million in complete liabilities. Its guide worth stands at $1.4 billion, implying a P/B a number of of two.4, which aligns with its sector’s median P/B of two.4.

Furthermore, I estimate DNLI’s newest quarterly money burn at $96.0 million, calculated by including its CFOs and Internet CAPEX. This means a comparatively wholesome money runway of two.3 years. It’s price mentioning that Q2 2024 wasn’t an outlier quarter, and DNLI has been persistently burning its money at an analogous fee for the previous a number of quarters. Evidently, DNLI appears to be aggressively investing in pushing ahead its analysis.

Supply: Company Presentation. August 2024.

For my part, DNLI’s superior transport applied sciences are versatile, enabling software throughout a variety of potential indications. This flexibility opens the door to partnerships and potential revenues from royalties or milestone funds. Whereas the know-how is promising, drug approvals are nonetheless a 12 months or extra away, even beneath probably the most optimistic assumptions. Thus, DNLI is certainly racing in opposition to the clock, however I lean bullish on the inventory as a result of its affordable valuation and uniquely disruptive TV platform.

Funding Caveats: Danger Evaluation

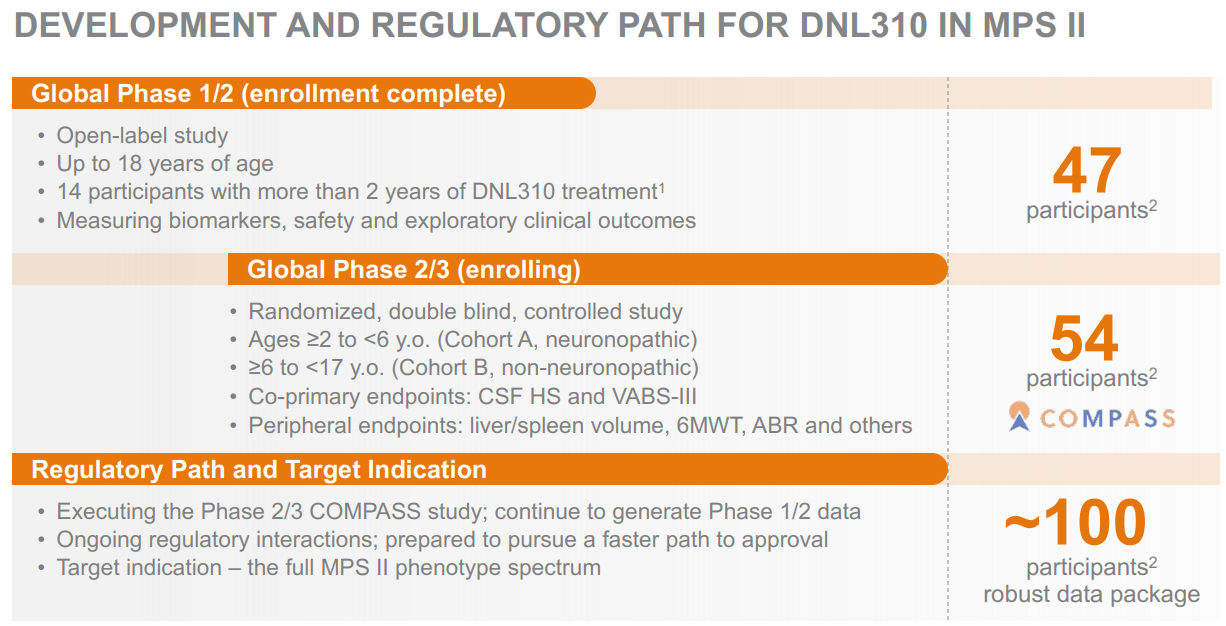

I feel DNLI’s funding thesis largely hinges on its platform’s potential. If the corporate fails to persuade regulators that it’s secure and efficient, basically all of its IP would endure. Furthermore, even when one in every of its drug candidates reaches approval, it could nonetheless face appreciable competitors. For instance, DNL310 for MPS II is one in every of DNLI’s main drug candidates as a result of its promising preliminary information. Additionally, DNL310 has a comparatively stable aggressive profile, as the usual MPS II enzyme alternative therapies don’t cross the BBB.

Nevertheless, REGENXBIO (RGNX) has an adeno-associated virus [AAV] vector in medical trials, which may compete with DNL310. I imagine DNL310’s prospects are in all probability superior, however the level is that it’s unlikely it could grow to be the brand new customary of care instantly. Sadly, we are able to’t dismiss the truth that clinical-stage biotech is commonly a recreation in opposition to time, corresponding to money reserves operating out. On the similar time, DNLI’s platform is clearly relevant throughout a number of doable CNS indications.

Supply: TradingView.

This makes pricing DNLI difficult as a result of, on one aspect, there’s a probably disruptive biotechnology platform with wide-ranging purposes. However, there are nonetheless no product gross sales, and the money burn stays comparatively excessive. Nonetheless, I lean in the direction of a bullish ranking as a result of its distinctive know-how platform, particularly after its $500 million increase, corroborating institutional buyers’ perception in its know-how. With such huge backing, DNLI has sufficient sources to show its analysis on not less than one in every of its a number of promising drug candidates. I imagine a single drug approval would derisk DNLI significantly, as it could additionally validate its platform as an entire.

DCA Purchase: Conclusion

Total, DNLI is usually a guess on its promising TV platform. Nevertheless, DNLI just isn’t a short-term guess, and I feel there’ll probably be many pullbacks till it has an accredited drug. So, I wouldn’t advise shopping for your whole place directly. As a substitute, I counsel a measured DCA technique for DNLI. Over time, I imagine its analysis will ship, however buyers have to be ready for a bumpy experience, primarily as a result of its comparatively excessive money burn. Thus, a DCA method will give buyers a stake in its upside potential with out overcommitting to a inventory which may commerce sideways till it will get a transparent path to approval on one in every of its a number of drug candidates. Nevertheless, as soon as DNLI obtains approval for one in every of them, it may utterly change its danger profile and validate its know-how. Since I feel DNLI has sufficient sources to do that, I imagine it’s truthful to fee it DCA “purchase” for buyers who perceive the inherent biotech dangers.

{kind=link}